Weekly Market Commentary - July 5, 2026

As we turn the page on the second quarter and celebrate America's 250th birthday, U.S. equity markets delivered a resilient performance amid a complex backdrop of strong corporate earnings, moderating economic data, geopolitical undercurrents, and sector rotation. The S&P 500 capped its best quarter since 2020 with a roughly 15% total return (including dividends), while the Dow Jones Industrial Average pushed to fresh record closes near 52,300.

This week’s holiday-shortened trading saw mixed but generally constructive action. Dip-buying supported major averages after last week’s consolidation, with the Dow posting modest gains early before closing near flat. The S&P 500 and Nasdaq experienced some profit-taking in technology names, but broader participation and international strength underscored a healthy broadening of the rally.

Our proprietary quantitative framework—refined over 23+ years—continues to highlight positive earnings revision momentum, particularly in AI-enabled leaders, balanced against valuation discipline and risk management. Markets are climbing a wall of worry, as they often do, rewarding those focused on fundamentals over headlines.

Macro Backdrop: Resilient Growth with Cooling Signals

U.S. economic data painted a picture of steady expansion rather than overheating. The latest jobs report came in softer than expected, tempering expectations for an imminent Federal Reserve rate hike and reinforcing a soft-landing narrative. This shift helped stabilize bond yields and supported risk assets.

Inflation pressures have eased notably from peak levels, aided by declining oil prices as geopolitical risk premiums fade. Brent crude and WTI have pulled back amid improved supply flows through key chokepoints like the Strait of Hormuz and expectations of adequate global inventories. While energy remains sensitive to developments in the Middle East, the overall commodity backdrop is less inflationary than feared earlier in the year.

Looking ahead, the week of July 6–10 brings key reads on services PMI, ADP employment, FOMC minutes, jobless claims, and existing home sales. These will provide further clarity on labor market health and monetary policy trajectory. Consensus expectations point to continued double-digit S&P 500 earnings growth for 2026, with AI productivity gains providing a measurable tailwind.

Earnings Momentum: AI as a Support Layer, Not the Whole Story

Corporate America is delivering. Q2 2026 earnings growth estimates have been revised higher, tracking around 23% year-over-year in recent updates—well above initial forecasts. Upward revisions are most pronounced in Technology, Communication Services, and select cyclicals, driven by AI capital spending, cloud expansion, and operational efficiencies.

Our “numbers-first” approach—centered on earnings revisions as key buy/sell signals—remains constructive. AI momentum screening, combined with fundamental verification and trend confirmation, continues to identify high-quality compounders. The Magnificent Seven and AI hyperscalers have shouldered much of the earnings load, but we are seeing encouraging breadth in areas like financials, industrials, and infrastructure plays tied to data centers and energy transition.

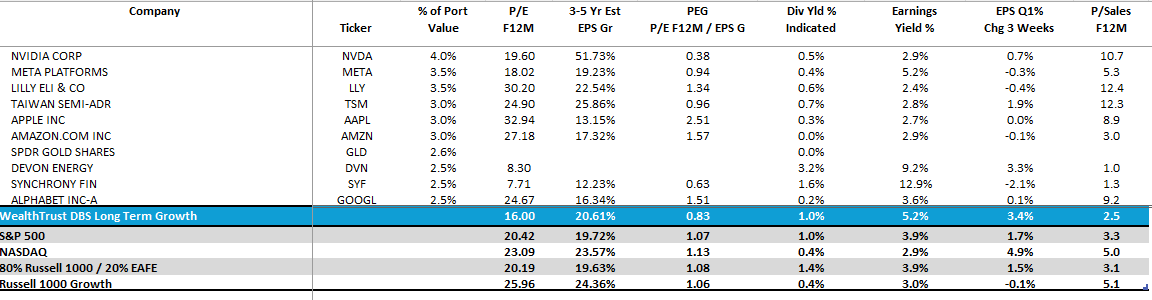

Valuations are elevated in leadership names, but the earnings trajectory supports current multiples for those executing well. Our Great 38 Core / Term Growth Strategies (maintain a disciplined blend: quantitative rigor, momentum confirmation, and active sell rules to protect capital during rotations).

Sector rotation remains a dominant theme. Technology pulled back modestly amid profit-taking in semiconductors, while financials and other “old economy” names gained traction. International and emerging markets also showed strength, capping solid quarterly results. This broadening is a positive development for sustained bull market health.

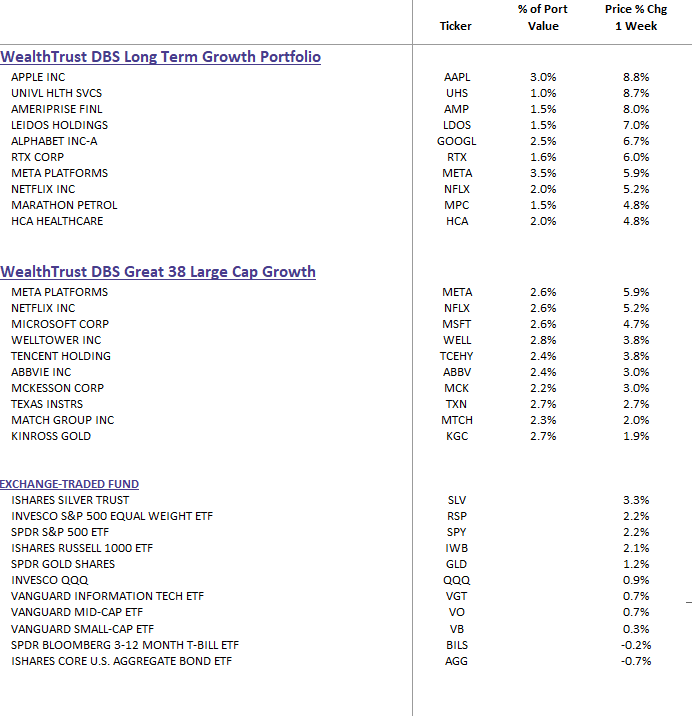

DBS Long-Term Growth & DBS Great 38 Large Cap Growth Top Ten and Benchmark Weekly Performance Summary:

WealthTrust DBS Long Term Growth Portfolio | Top 10 Equity Review

Geopolitics and Risks: Navigating Uncertainty

Geopolitical tensions—particularly in the Middle East—continue to influence sentiment and commodity prices, but markets have demonstrated remarkable resilience. Reduced risk premiums in oil and signs of diplomatic progress have helped stabilize energy markets. Broader global equity indices, including those in Asia and Europe, benefited from this relative de-escalation.

We remain vigilant on tail risks: potential flare-ups, policy shifts, or surprises in upcoming data. However, corporate balance sheets are strong; fiscal support is front-loaded in places, and AI-driven productivity should provide a multi-year growth engine. Our risk management overlays—tactical hedging and sector positioning—aim to mitigate downside while capturing upside.

Portfolio Implications and Outlook

For investors, the message is one of disciplined optimism. The first half of 2026 has been strong, with the Dow surpassing the 50,000 milestone earlier this year and major indices delivering robust returns. Yet sustainability depends on continued earnings delivery, controlled inflation, and measured Fed policy.

Key Watchpoints for Clients:

- Earnings Season Ramp-Up: Focus on AI monetization, margin resilience, and guidance breadth.

- Rotation Opportunities: Diversification beyond mega-cap tech into quality names with attractive revisions and valuations.

- Income and Alternatives: Balanced allocations, including our Core/Growth Blend strategies, for multi-generational wealth planning.

- Tax Efficiency: Opportunities in capital loss harvesting, Roth strategies, and deferred sales trusts remain relevant in this environment.

At WealthTrust Asset Management, our hybrid RIA model combines proprietary quantitative and fundamental research with direct portfolio manager access. Strategies like the DBS Long Term Growth, and balanced offerings are designed to help clients sleep better at night—with the goal of delivering outperformance through disciplined active management.

We are actively engaged in platform integrations, TAMP partnerships, and strategic conversations to expand access to these institutional-grade solutions.

Bottom Line: Markets have rewarded adaptability and a focus on fundamentals. With positive earnings momentum, broadening participation, and a resilient macro foundation, the path higher remains intact—provided we maintain sell discipline and risk awareness. As always, we prioritize transparency, education, and long-term compounding for our clients nationwide.

John G. McHugh, CPA President & Chief Investment Officer WealthTrust Asset Management LLC Destin, Florida

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. This commentary is for informational purposes only and does not constitute investment advice. Please consult your advisor for personalized guidance. GIPS-verified strategies; Morningstar ratings as of recent evaluation.