Weekly Market Commentary: Week Ending June 13, 2026

Markets delivered another chapter of volatility this week, but the underlying tone turned more constructive by Friday. After testing resolve with a sharp mid-week pullback in technology and semiconductors, equities rebounded on growing signs that the most acute phase of Middle East supply disruptions may be easing. The S&P 500 closed the week near 7,431, recovering from an intraday low around 7,257 earlier in the period and remaining well above the March lows. The Dow Jones Industrial Average held near the 50,800–51,200 zone, while the Nasdaq Composite showed particular resilience in the final sessions as chip stocks stabilized.

Year-to-date, major benchmarks remain solidly positive, with the S&P 500 up approximately 8.5% and the Nasdaq still showing double-digit gains despite the recent digestion. Breadth has improved relative to the concentrated leadership of earlier in the year, a development our quantitative models view favorably.

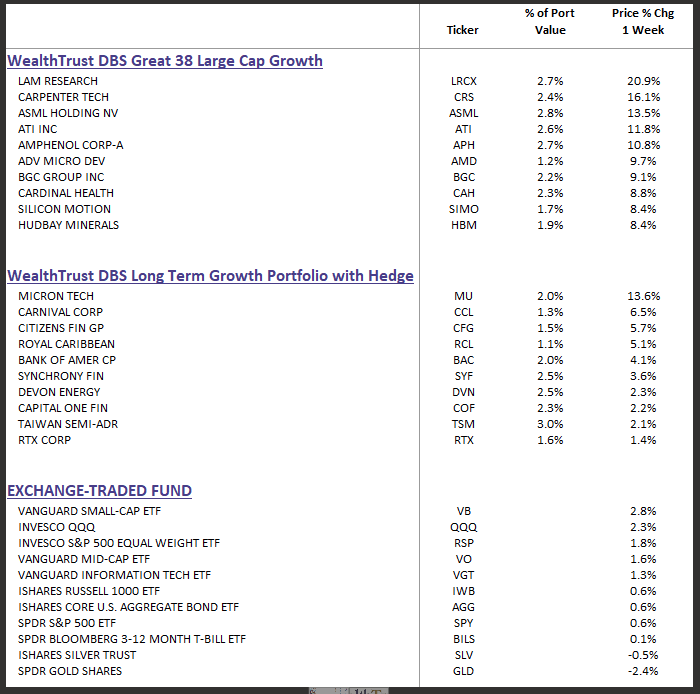

DBS Great 38 Large Cap Growth & DBS Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

For those interested in the WealthTrust DBS Great 38 Strategy, it is currently recommended for new accounts of accredited investors with $1 million or more in liquid assets.

In addition, the strategy is also well-suited as a core/growth allocation by combining 50% in the DBS Long Term Growth Strategy (core) with 50% in the DBS Great 38 Strategy (growth).

Geopolitical De-escalation Signals and Oil’s Sharp Reprieve

The dominant macro story remains the evolving situation around the Strait of Hormuz. After months of elevated risk premium that pushed Brent crude above $100/bbl and WTI into the mid-$90s at times, prices have retreated meaningfully. As of Friday’s close, Brent traded near $86–87/bbl and WTI around $84–88/bbl — still elevated on a year-to-date basis but down sharply from recent peaks. Reports of increasing ship traffic through the strait, combined with diplomatic language suggesting potential pathways toward normalization, triggered a rapid compression of the geopolitical risk premium.

This matters beyond energy prices. Lower oil directly eases one of the stickier components of the recent inflation uptick. May CPI came in at 4.2% year-over-year, with energy costs a visible contributor. Core measures also firmed, though the trajectory of headline inflation will likely improve if energy prices remain contained. Markets are now pricing a higher probability that the Federal Reserve stays on hold at its June 17–18 meeting, with the target range remaining 3.50%–3.75%. A growing number of economists see rates unchanged through year-end, reflecting both resilient growth and persistent (if moderating) price pressures.

For our process, the key is not to overreact to any single headline but to monitor how these macro shifts flow through earnings revisions and sector leadership. Energy names that benefited from the earlier spike have seen some profit-taking, while sectors sensitive to lower input costs and improved consumer purchasing power have found support.

Earnings Power and the AI Investment Cycle Remain Intact

Corporate America continues to deliver. Forward earnings estimates for the S&P 500 remain robust, with 2026 EPS projections in the $340 area, according to recent Wall Street updates — implying strong double-digit growth. The AI capital expenditure cycle shows no signs of meaningful deceleration. Companies across the technology stack and beyond continue to invest aggressively in infrastructure, software, and applications. This is not merely narrative; it is visible in order books, guidance, and the sustained outperformance of companies demonstrating real monetization traction.

That said, the market has become more discerning. The sharp one-day semiconductor drawdown earlier in the period (with over $1 trillion in market cap erased in a session at one point) reflected classic profit-taking after an extended run rather than a fundamental breakdown. Our AI momentum screening combined with fundamental verification helped identify areas of overcrowding and valuation compression in real time. The rebound in chip names by week’s end underscores that the underlying demand story remains intact, even as investors rotate toward names with clearer near-term earnings visibility and more reasonable valuations.

Quantitative Signals: Earnings Revisions and Breadth

Our proprietary framework continues to emphasize earnings revisions as the highest-conviction signal. In environments like this — where macro crosscurrents (geopolitics, inflation, Fed policy) create noise — companies that consistently beat and raise estimates tend to outperform over time. Our three-fold verification process (AI-generated candidates, quantitative/fundamental overlay, and momentum confirmation) has been particularly useful in navigating the recent rotation.

We are also seeing early signs of improved market breadth. While mega-cap technology remains a powerful driver, participation from mid- and small-cap names, financials, and select industrial and consumer sectors has increased during relief rallies. This aligns with our long-standing view that durable advances are rarely sustained by a handful of names alone. The WealthTrust DBS Long Term Growth Strategy and our blended approaches (including the Core/Growth Blend) are designed to capture both the secular AI theme and the broader earnings expansion that typically follows periods of volatility.

Valuation multiples have compressed modestly from their peaks. The S&P 500 forward P/E now sits closer to long-term averages after the recent digestion. This creates a healthier setup for active managers who can identify mispricings created by headline-driven swings.

Risks Worth Monitoring

We remain vigilant on several fronts:

- Inflation persistence: Even with lower oil, shelter and services components could keep core readings elevated longer than hoped.

- Geopolitical re-escalation risk: Any reversal in Hormuz traffic or diplomatic progress could quickly reintroduce volatility.

- Policy uncertainty: The June FOMC meeting and subsequent data (including June employment and inflation prints) will set the tone for the second half.

- Valuation pockets: Areas that ran hardest earlier in the year remain vulnerable to further mean-reversion if earnings delivery disappoints.

Our sell discipline — rooted in earnings revision deterioration and momentum breakdown — is designed to manage these risks without abandoning the primary growth drivers.

Positioning and the Path Forward

We continue to favor a balanced, active approach. The combination of secular growth exposure (via AI and technology leaders that meet our quantitative thresholds) with high-quality businesses showing earnings momentum across sectors provides both upside participation and downside ballast. Blended allocations — for example, meaningful exposure to the Long Term Growth framework — have historically delivered attractive risk-adjusted outcomes by reducing single-strategy concentration while maintaining growth bias.

International and emerging markets have also participated in recent relief moves, particularly as lower oil supports certain economies. We maintain selective exposure where our models identify improving revision trends and reasonable valuations.

Next week brings the FOMC decision, more earnings reports, and continued monitoring of global shipping and diplomatic developments. We expect volatility to persist, but the foundation of strong corporate earnings and ongoing AI-driven investment gives us confidence that the longer-term trajectory remains upward — provided investors stay disciplined and avoid chasing or panicking at extremes.

Markets do not move in straight lines. The recent pullback and subsequent recovery reinforce the value of a rules-based, numbers-first process over reactive narratives. Our role is to help you stay positioned for the opportunities while managing the inevitable bumps along the way.

As always, I welcome your questions and look forward to speaking you.

John, coming to you from Destin, Florida

President & Chief Investment Officer WealthTrust Asset Management LLC

This commentary is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Please consult your financial advisor regarding your specific situation. GIPS® verification applies to certain strategies; additional details available upon request.