Weekly Market Commentary: Week Ending June 6, 2026

Executive Summary

Financial markets delivered a tale of two halves this week. The S&P 500 reached fresh record highs mid-week on resilient AI-driven earnings and hopes for de-escalation in the Middle East, only to give back gains sharply on Friday amid a steep selloff in semiconductors and hotter-than-expected jobs data that pushed Treasury yields higher.

The index closed the week around 7,384, down roughly 2.5% for the period after touching intraday highs near 7,621. The Nasdaq fared worse, declining over 4%, while the Dow showed relative resilience. Oil prices moderated from recent peaks as diplomatic signals around the Strait of Hormuz improved, but volatility remains elevated.

Our proprietary quantitative framework continues to highlight earnings revisions and momentum as key signals. While the AI theme remains a powerful secular driver, broadening leadership into financials, industrials, and energy underscores the importance of disciplined sector rotation and risk management in this environment. (see weekly performance summary below)

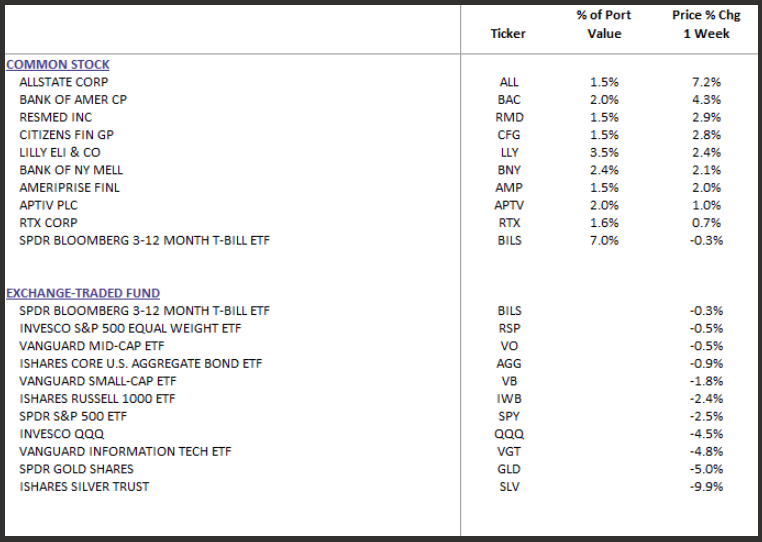

DBS Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

Macro and Geopolitical Backdrop

Geopolitical tensions centered on the Middle East dominated headlines. The partial or threatened closure of the Strait of Hormuz—through which roughly 20% of global oil and LNG typically flows—drove oil prices higher earlier in the period, with Brent crude briefly trading in elevated ranges before easing on reports of potential U.S.-Iran progress and reopening hopes. Prices settled near $90-95/bbl by week's end, still reflecting supply concerns but down from worst-case fears.

U.S. economic data painted a picture of resilience with pockets of pressure. May's nonfarm payrolls surprised to the upside with 172,000 jobs added—well above expectations—while wage growth remained firm. This cooled rate-cut expectations and lifted the 10-year Treasury yield toward 4.5%. Inflation readings have ticked higher due to energy pass-through, with headline CPI around 3.8% in recent data.

Real GDP growth for Q1 2026 came in at a solid 1.6% annualized pace. Forward estimates for full-year 2026 hover in the 2.0-2.5% range, supported by consumer spending and investment but tempered by higher energy costs and policy uncertainties.

The Federal Reserve remains data-dependent, balancing inflation risks from energy shocks against a still-healthy labor market. Our models suggest any pause in easing will be temporary if growth holds and geopolitical risks subside.

Market Performance and Sector Dynamics

- Broad Indices: S&P 500 YTD gains remain positive, but the week highlighted concentration risks. The equal-weight S&P and small-caps (Russell 2000) showed mixed results amid rotation.

- Technology & AI: Strong earnings from key players reinforced AI capital spending momentum, but late-week profit-taking in chips (e.g., Broadcom, Nvidia-related names) triggered a sharp reversal. The Philadelphia Semiconductor Index swung notably. AI remains a core growth driver, powering data centers and productivity gains, but valuations demand scrutiny.

- Rotation Winners: Financials, energy, industrials, and defensives outperformed on a relative basis. Higher yields and a steeper curve support bank net interest margins. Energy benefits from elevated oil prices and infrastructure demand tied to AI power needs. Old-economy revival themes—evident in materials and select cyclicals—align with our sector rotation signals.

Earnings and Corporate Fundamentals

Corporate America continues to deliver, particularly where AI intersects with real-world capex. Semiconductor and related names posted robust results tied to data center buildouts, validating our long-term view on technological disruption. However, forward guidance and margin pressures in some segments contributed to the late-week volatility.

Our "numbers first" approach—focusing on earnings revisions, quantitative screens, and momentum—identified opportunities in diversified holdings. The Great 38 Core strategy and WealthTrust DBS Long Term Growth continue to emphasize high-quality companies with strong fundamentals, downside protection, and growth potential. Blended allocations (e.g., 50/50 Core/Growth) provide balanced exposure.

Valuations: S&P 500 forward P/E remains elevated but supported by earnings growth expectations in the double-digits for key sectors. We monitor P/E and P/S compression risks closely, especially in high-momentum names.

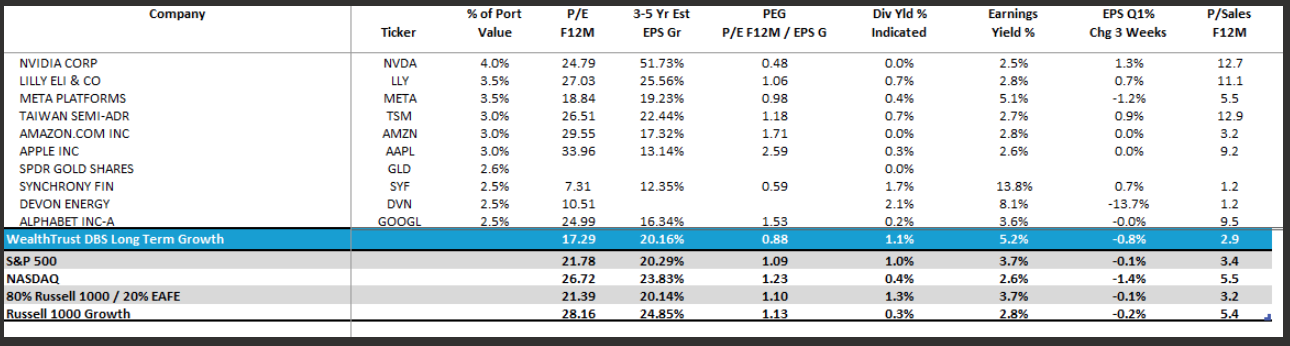

WealthTrust DBS Long Term Growth Portfolio | Top 10 Equity Review

Investment Implications and Risk Management

- Stay Disciplined on Sell Rules: Earnings revisions remain our primary sell/buy signals. We favor active management with clear risk parameters over passive exposure.

- Diversification Matters: The week's rotation reinforces the value of our hybrid AI + quantitative methodology. Overweight quality financials, energy/infrastructure plays, and select industrials for balance against tech concentration.

- Geopolitical and Inflation Watch: Monitor Strait of Hormuz developments and energy prices. Tactical hedging and inflation-protected positioning (within limits) help clients "sleep better at night."

- Opportunity in Volatility: Pullbacks create entry points for accredited investors in GIPS-verified strategies, available via TAMPs and platforms including SMArtX and others.

At WealthTrust, our proprietary framework—refined over decades and augmented by AI as a support layer—prioritizes capital preservation alongside growth. Historical examples, such as our 2007 GE call, underscore the edge of numbers-driven decisions amid uncertainty.

Outlook

Markets have proven resilient, climbing to new highs on AI tailwinds and economic strength despite geopolitical friction. Near-term volatility from yields, energy, and sector rebalancing is likely, but the secular backdrop—AI productivity gains, corporate investment, and U.S. economic adaptability—supports a constructive longer-term view.

We remain focused on multi-generational wealth planning, tax efficiency, and fiduciary outcomes. For clients and prospects, this environment rewards disciplined, transparent active management.

As always, we welcome conversations about integrating our strategies—whether via SMAs, or partnership opportunities. Contact us to discuss how our approach can support your objectives.