Weekly Market Commentary: Week Ending May 23, 2026

U.S. equities extended their remarkable winning streak this week, with the S&P 500 on track for its eighth consecutive weekly gain—the longest run since late 2023. Markets showed resilience amid geopolitical tensions in the Middle East, persistent inflation pressures, and a cautious Federal Reserve. Tech and AI-related stocks continued to lead, while broader participation emerged in sectors like healthcare. Bond yields remained relatively stable but reflected ongoing rate vigilance. Oil prices fluctuated with supply concerns, gold held firm as a safe haven, and Bitcoin traded in a volatile range. Overall, strong corporate earnings and AI optimism outweighed near-term headwinds, though investors remain watchful of inflation and global risks.

This week’s developments reinforce a narrative of resilient growth supported by business investment and technological innovation, even as supply-side risks from geopolitics add complexity.

Equity Markets: Bulls in Control

Major U.S. indices posted solid gains for the week. The S&P 500 rose approximately 0.9%, closing near record levels and extending its streak. The Dow Jones Industrial Average climbed about 2.1% (with a strong Friday session adding nearly 300 points to a new record close around 50,580), while the Nasdaq Composite gained roughly 0.5%.

Key drivers:

- AI and Tech Momentum: Continued enthusiasm for artificial intelligence fueled gains, with hyperscalers and related firms delivering strong results. Nvidia’s positive earnings (noted as a bellwether) remained a focal point.

- Earnings Resilience: Corporate America’s reporting season highlighted durability, particularly in technology and selective industrials. Apple, for instance, provided upbeat forecasts earlier in the period.

- Broader Participation: Healthcare emerged as a standout, on track for its best weekly performance in months, adding balance beyond the "Magnificent Seven."

International markets showed mixed results. European indices edged higher amid steadier central bank policies, while Asian markets benefited from tech strength despite regional uncertainties.

Small-cap stocks performed extremely well, reflecting rotation dynamics.

Fixed Income and Monetary Policy: Steady but Watchful

The Federal Reserve maintained its target range for the federal funds rate at 3.5%–3.75% following the April meeting, with notable dissent (an 8-4 vote, the highest since 1992). Minutes from the meeting revealed that a majority of officials signaled openness to policy firming if inflation persists above the 2% target.

Treasury yields moved modestly, with the market digesting hotter-than-expected April inflation data (headline CPI up significantly year-over-year, partly due to energy and a shelter adjustment). Retail sales remained positive, underscoring consumer resilience despite bifurcated spending patterns (stronger among higher-income households).

Bond markets provided some ballast, with income supporting returns in fixed income amid equity volatility. However, fiscal concerns and inflation risks kept pressure on longer-duration assets. Markets have largely priced out near-term rate cuts, with expectations now leaning toward stability or potential hikes later in 2026–2027 depending on data evolution.

Commodities: Energy in Focus

Oil remained elevated but volatile. Brent crude hovered above $100 at points amid Middle East tensions (impacting shipping and supply routes), though it pulled back below that level at times on ceasefire hopes or demand nuances. Geopolitical risks are estimated to subtract modestly from Q2/Q3 GDP via higher costs, but business investment (AI infrastructure, reshoring, automation) offers a counterbalance.

Other commodities reflected mixed supply-demand dynamics, with industrial metals tied to AI and infrastructure themes showing underlying support.

Cryptocurrency: Volatile but Resilient

Bitcoin traded around the $75,000–$80,000 range, experiencing swings typical of the asset class. It remains sensitive to risk sentiment, macroeconomic data, and correlations with tech equities. While not at all-time highs, the longer-term bullish case tied to institutional adoption and scarcity narratives persists amid broader market optimism. We believe it's better to own Crypto infrastructure companies.

Economic Backdrop and Outlook

The U.S. economy demonstrates resilience. Q1 GDP came in around 2%, with non-residential fixed investment (tech, equipment, automation) contributing meaningfully. Consumer spending holds up, though low savings rates and credit reliance among lower/middle-income households warrant monitoring.

Inflation remains the primary vulnerability—April’s print showed stickiness, particularly in energy and shelter components (the latter partly a data catch-up effect). Geopolitical factors add supply-side pressure, but core growth drivers like AI capex could sustain expansion for several quarters, echoing 1990s dynamics.

Looking Ahead:

- Focus shifts to upcoming data releases (housing starts, consumer sentiment) and corporate earnings.

- Nvidia’s report was excellent, but the stock did not participate in the rally. We believe the fear of competition is overstated.

- Potential U.S.-Iran peace developments or escalations will influence energy markets and risk appetite.

Key Risks

- Inflation Resurgence: Persistent or worsening price pressures could force a more hawkish Fed posture.

- Geopolitics: Escalation in the Middle East remains a wildcard for energy prices, inflation, and growth.

- Valuations: Extended multiples in tech/AI require sustained earnings delivery to justify.

- Consumer Health: Thinner household buffers could amplify any slowdown.

Investment Implications

Markets reward selectivity. AI-driven productivity gains and corporate investment provide a strong fundamental backdrop, supporting a constructive equity outlook over the medium term. Diversification across sectors, quality fixed income for ballast, and tactical exposure to commodities/gold for hedging make sense. Long-term investors should view volatility as an opportunity rather than a deterrent, staying focused on durable growth themes.

This environment favors active management and a balanced portfolio. As always, individual circumstances should guide allocations.

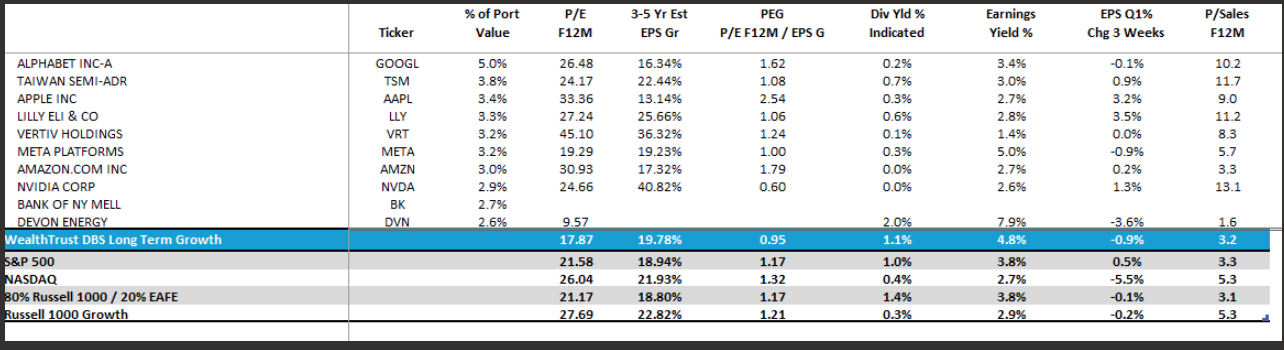

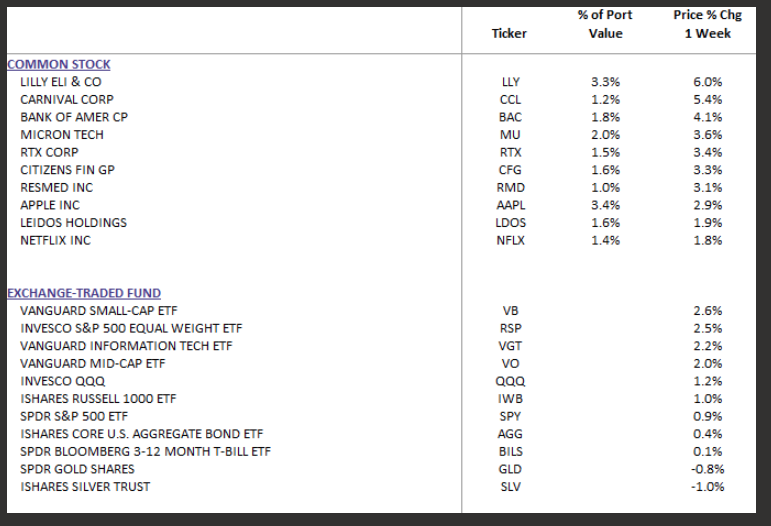

DBS Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

DBS Long Term Growth Portfolio | Top 10 Equity Review