Weekly Commentary for the week ending May 9, 2026

U.S. equity markets extended their winning streak to six consecutive weeks, with major indexes closing near or at record highs. Technology and growth stocks drove gains, while broader participation remained selective. Geopolitical developments in the Middle East dominated headlines, causing oil price swings, but markets largely looked through near-term uncertainty toward strong corporate earnings and economic resilience.

Equity Markets: Tech-Led Rally Hits New Highs

The S&P 500 rose about 2.4% for the week (depending on exact close), closing around 7,230–7,399, setting fresh records. The Nasdaq Composite outperformed with gains near 4.0%, closing above 25,000–26,000 at points and posting its strongest six-week stretch since 2009. The Dow Jones Industrial Average lagged modestly, up ~0.5%, closing near 49,500. Small caps (Russell 2000) added ~1.2% and also hit new highs.

Sector leadership stayed concentrated in Technology, Communication Services, and Consumer Discretionary , all benefiting from mega-cap exposure. . The rally, which began in late March after earlier volatility, reflected investors prioritizing fundamentals over geopolitical noise. Energy outperformed at times on oil strength but gave back gains as prices eased. Laggards included Health Care and Financials, pressured by policy and rate dynamics. Six of eleven S&P sectors finished the week lower or flat, underscoring the narrow breadth. This should set up a rotation back into these underperforming sectors.

Key drivers:

- Strong Q1 earnings from Magnificent 7 and hyperscalers (Alphabet, Amazon, Meta, Microsoft, Apple). Revenue and EPS beats were widespread, with AI capital expenditure surging—Meta guiding capex to $125–145B, Microsoft spending ~$32B in one quarter. Combined cloud/AI infrastructure spend projections exceeded $660B for 2026.

- Progress toward a U.S.-Iran framework deal, which eased some risk premium and triggered a sharp oil pullback.

- Resilient Q1 GDP (+2.0% annualized) and labor data.

Volatility (VIX) eased toward the mid-teens, reflecting improved sentiment.

Fixed Income: Yields Mixed, Modest Gains

Bonds produced modest positive returns as rates drifted lower late in the week. The Bloomberg U.S. Aggregate Index was roughly flat to slightly up. Treasury yields ended with the 10-year around 4.37–4.39%, 2-year near 3.90%, and 30-year testing but retreating from 5% levels. Corporate and high-yield spreads remained contained.

The Federal Reserve held the federal funds rate at 3.50–3.75% in its April meeting, with notable dissent (four members, highest since early 1990s). Three opposed the easing bias in the statement; one favored an immediate cut. Policymakers cited oil-driven inflation risks and a still-solid economy. Markets now price no cuts through much of 2026, with the first possibly late in the year.

Higher oil and fiscal borrowing concerns kept longer-term yields elevated at points, pressuring duration-sensitive assets.

Commodities and Currencies: Oil Volatility in Focus

Oil was the week's biggest mover. WTI traded as high as the mid-$100s+ amid Hormuz tensions and attacks but fell sharply (>8–10%) on de-escalation hopes, ending around $90–106. Brent followed suit. Gasoline prices stayed elevated for consumers.

Gold held near elevated levels (~$4,600–4,637/oz) but faced pressure from rising yields and a stronger dollar at times. It benefited earlier from safe-haven demand.

Bitcoin traded around $79,000–82,000, showing resilience but underperforming some risk assets amid macro crosscurrents.

The U.S. dollar was mixed but generally firm on higher-for-longer rate expectations.

Economic Backdrop: Solid but Watchful

- Q1 GDP: +2.0% annualized rebound, driven by business investment (AI-related), inventories, and government spending.

- Labor Market: April jobs report showed resilience (better-than-expected adds, unemployment steady ~4.3%). Initial claims low.

- Inflation: PCE and other readings sticky; oil pass-through remains a risk.

- Broader global equities mixed-positive, with emerging markets and select developed indices (e.g., South Korea) showing strength.

The economy demonstrated the ability to absorb geopolitical shocks so far, thanks to diversified energy and strong corporate balance sheets.

Outlook and Risks

Markets have shown remarkable resilience, pricing in a "soft landing plus" scenario where AI productivity gains offset higher energy costs. Earnings growth remains robust (S&P 500 Q1 on track for double-digit+), supporting valuations despite elevated multiples in growth segments.

Bull Case: Iran deal materializes → lower oil → reduced inflation pressure → eventual Fed easing. AI capex cycle continues driving earnings. Broadening participation lifts small/mid-caps.

Bear Case: Geopolitical breakdown reignites oil spike and inflation. Sticky prices delay cuts. Narrow breadth leaves the market vulnerable to rotation or profit-taking. Fiscal deficits and supply keep yields elevated. This is why we have maintained liquidity (BILS Short Term Treasury Bonds)

Base Case (Most Likely): Grinding higher with volatility. Markets continue rewarding earnings delivery over macro noise. Expect rotation opportunities as energy normalizes, and rate sensitivity plays out. Valuations are full but supported by growth. This is our opinion by looking for opportunities to deploy our liquidity during potential volatile periods.

Investor Implications:

- Maintain equity exposure with quality and diversification bias.

- Fixed income for ballast—intermediate duration offers yield without excessive rate risk.

- Commodities/energy as tactical hedges or inflation plays.

- Rebalance toward areas of broadening strength.

- Cash/dry powder for dips.

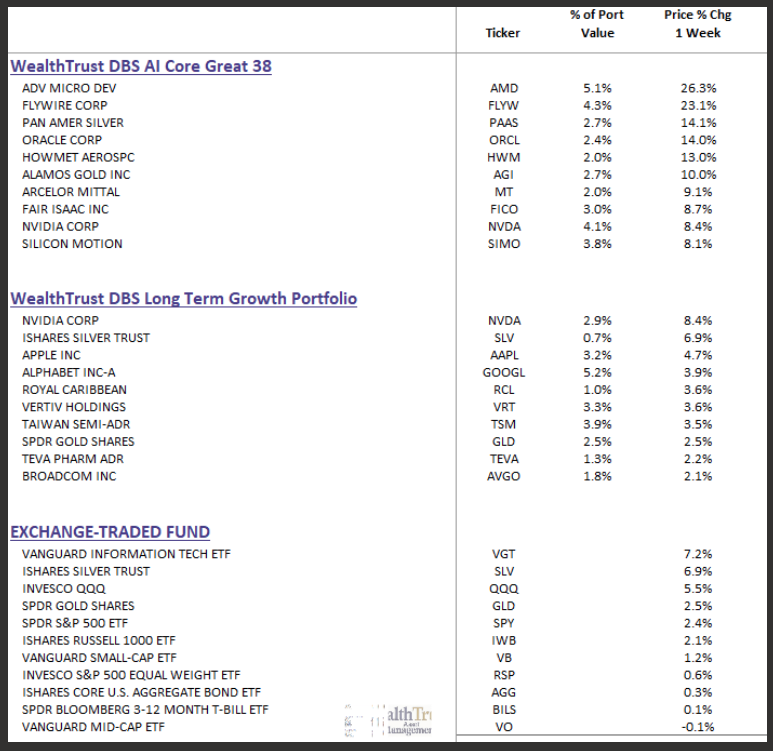

The Great 38 Strategy Introduction

WealthTrust has developed a new strategy, The Great 38. It is something I’m really excited about. It combines our AI Momentum Review and Quantitative Review with an AI-powered CFA skill-set overlay. It’s designed as if a full team of CFAs had thoroughly reviewed thousands of companies and hand-selected the 38 strongest ones.

The Great 38 is an actively managed strategy designed for long-term capital growth. It invests in a focused portfolio of up to 38 primarily large-cap individual equities, selected through quantitative screening, disciplined portfolio construction, and rigorous CFA-style fundamental review.

The process identifies companies with strong earnings, momentum, attractive valuations, quality characteristics, and favorable risk-adjusted potential. Each holding is evaluated for a clear investment thesis, competitive positioning, management quality, key risks, and portfolio fit.

The portfolio targets ~99% equity exposure and maintains an intermediate- to long-term horizon with tactical flexibility and controlled turnover.

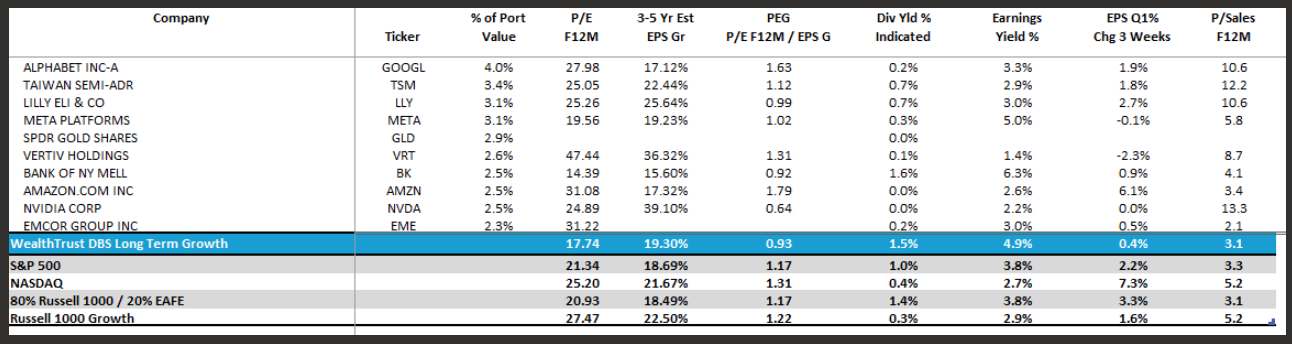

DBS Great 38 and Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

DBS Long Term Growth Portfolio | Top 10 Equity Review