Weekly Commentary for the week ending May 2, 2026

U.S. equities capped another strong week, extending gains for the fifth straight session as investors prioritized robust corporate earnings and signs of potential de-escalation in the Middle East over persistent risks from elevated oil prices and fiscal concerns. The S&P 500 closed at a record of 7,230.12 on Friday, May 1, up about 0.29% for the day and roughly 0.9% for the week. The Nasdaq Composite surged to a new all-time high of 25,114.44 (+0.89% Friday, +1.1% weekly), driven by tech strength. The Dow Jones Industrial Average finished at 49,499.27, down slightly on the day but up ~0.5% for the week.

This performance marks a continuation of April’s powerful rebound—the S&P 500’s best monthly gain since November 2020 (around +10%)—as markets shook off earlier corrections tied to the Iran conflict. Breadth remained somewhat narrow, with mega-cap tech and select AI-related names leading, while small-caps (Russell 2000 +0.79% weekly) and value stocks showed mixed results.

Equities: Earnings Season Delivers, AI Capex Shines Through Noise

Corporate America’s Q1 reporting has been a standout, with blended earnings growth estimates now at +27.1% year-over-year (up from +13.1% at quarter-end) and revenue growth at +11.1%. Hyper scalers and Big Tech largely beat expectations, reinforcing the AI infrastructure buildout theme. Apple’s fiscal Q2 results (released late week) featured beats on earnings/revenue and a solid outlook, sending shares up over 3% and helping indices close higher despite mixed energy performance.

The “Magnificent Seven” and AI ecosystem provided the backbone: strength in semiconductors and capex guidance from major players offset jitters around OpenAI and broader AI monetization timelines. This focus allowed indices to power through geopolitical headlines, including U.S.-Iran rhetoric, disrupted Strait of Hormuz shipping, and canceled negotiations. Late-week reports of a fresh Iranian proposal helped sentiment improve.

International markets joined the advance modestly. Europe gained on steady central bank policy and easing oil pressure late in the week, while Asia extended tech-driven gains. MSCI EAFE rose ~0.47% weekly; emerging markets +0.50%. Year-to-date, U.S. large-caps remain leaders, but international and small-cap exposure has added diversification benefits amid narrow breadth.

Key Sector Moves (Approximate Weekly):

- Technology/Communication Services: Strong leadership.

- Energy: Volatile but net positive on oil strength earlier in the period.

- Defensive (Staples, Utilities): Relative resilience.

- Broader market: Average S&P 500 stock lagged mega-caps, highlighting concentration risks.

Fixed Income: Fiscal Concerns Weigh, Yields Tick Higher

Treasuries faced pressure from deficit worries and a resilient growth backdrop, though demand improved after softer March data. The 10-year U.S. Treasury yield hovered around 4.35-4.40% late in the week. Short-dated credit and high-quality investment-grade bonds offered better income with less duration risk.

The Fed held rates steady at 3.50%-3.75% in its late-April meeting, with notable dissent (highest since 1992), underscoring data-dependence amid sticky inflation and uncertainty. No cuts are priced in for the immediate horizon, with markets eyeing potential easing later in 2026.

Commodities and Currencies: Oil Dominates the Narrative

Oil prices remained elevated but pulled back late-week back on de-escalation hopes. Brent crude settled around $108-116/bbl. (volatile intra-week, with spikes above $120 earlier), while WTI traded lower. The Strait of Hormuz disruptions and regional production shut-ins have supported a sharp rally in energy, though a cooldown aided equity sentiment on Friday.

Gold and other safe-havens showed mixed moves as risk appetite returned. The U.S. dollar held firm on relative strength, while the yen rallied on intervention signals.

Macro Backdrop: Solid Data, Lingering Risks

U.S. economic resilience persists despite higher energy costs. Q1 GDP and other indicators showed steady expansion, with labor markets holding up. Upcoming data includes jobs reports, trade balance, and more earnings in the week of May 4-8. Inflation remains a watchpoint, but earnings growth is providing a buffer.

Geopolitics in the Middle East remains the wildcard—nine weeks into heightened conflict, nonlinear supply shocks are a rising concern, though markets have thus far demonstrated remarkable complacency.

Outlook: Momentum vs. Reality Checks

The bull case rests on continued earnings delivery, AI monetization progress, and any meaningful de-escalation in the Middle East that eases energy pressures. Valuation multiples are elevated, but supported by growth prospects (S&P 500 forward earnings trajectory improving). Risks include oil spiking on renewed disruptions, hotter inflation delaying Fed easing, or breadth deterioration if mega-caps falter.

Positioning Thoughts for Investors:

- Maintain core equity exposure with diversification beyond U.S. large-cap growth.

- Quality fixed income for ballast (short-intermediate duration).

- Energy/commodities as tactical hedges or inflation plays.

- Watch upcoming jobs data and earnings for confirmation of the soft-landing narrative.

Markets have climbed a wall of worry effectively in recent weeks, rewarding focus on fundamentals over headlines. However, with records being set and uncertainties unresolved, disciplined risk management remains essential. Volatility is likely to persist, but the earnings foundation appears solid enough to support further upside if geopolitical risks stabilize.

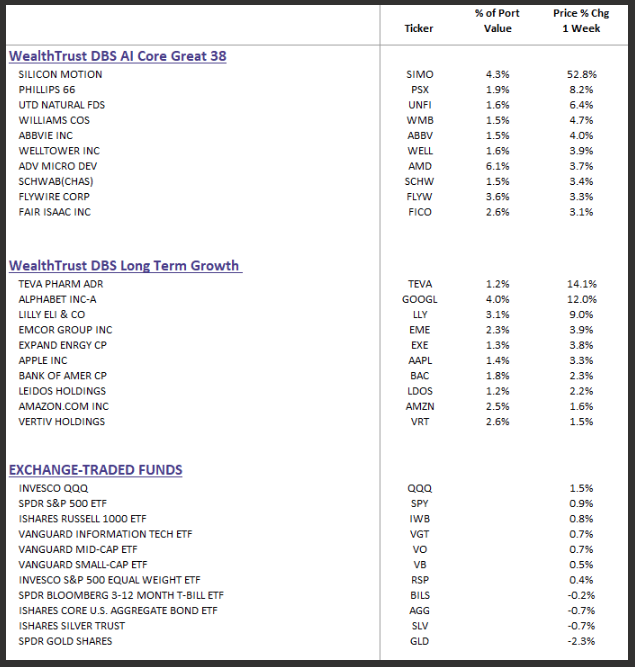

The Great 38 Strategy Introduction

WealthTrust has developed a new strategy, The Great 38. It is something I’m really excited about. It combines our AI Momentum Review and Quantitative Review with an AI-powered CFA skill-set overlay. It’s designed as if a full team of CFAs had thoroughly reviewed thousands of companies and hand-selected the 38 strongest ones.

The Great 38 is an actively managed strategy designed for long-term capital growth. It invests in a focused portfolio of up to 38 primarily large-cap individual equities, selected through quantitative screening, disciplined portfolio construction, and rigorous CFA-style fundamental review.

The process identifies companies with strong earnings, momentum, attractive valuations, quality characteristics, and favorable risk-adjusted potential. Each holding is evaluated for a clear investment thesis, competitive positioning, management quality, key risks, and portfolio fit.

The portfolio targets ~99% equity exposure and maintains an intermediate- to long-term horizon with tactical flexibility and controlled turnover.

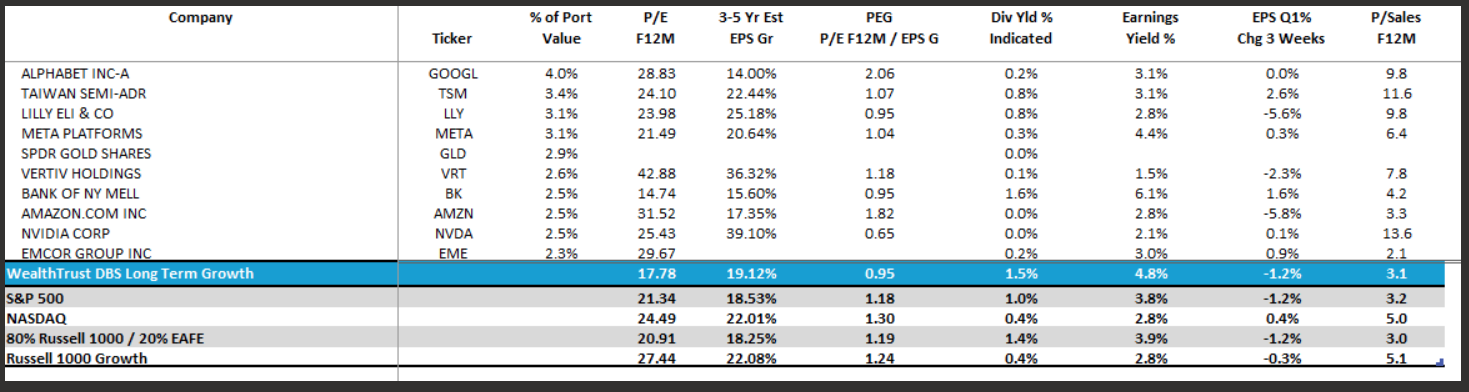

DBS Great 38 and Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

DBS Long Term Growth Portfolio | Top 10 Equity Review