Weekly Commentary for the week ending April 11, 2026

After weeks of geopolitical tension and market volatility tied to the U.S.-Iran conflict, investors got a much-needed breather this week. A surprise two-week ceasefire announcement between the United States and Iran—contingent on Iran reopening the Strait of Hormuz—triggered one of the strongest single-day rallies in nearly a year. Stocks surged mid-week; volatility eased, and oil prices pulled back sharply. Yet Friday’s mixed close and rising bond yields served as a reminder: this relief may be temporary, and markets remain on edge as high-level talks continue this weekend in Pakistan.

Equities: Strong Weekly Gains, But Friday Profit-Taking

Major U.S. indexes posted solid weekly advances, their best since November. The S&P 500 climbed roughly 3.7%, the Nasdaq Composite rose about 4.7%, the Dow Jones Industrial Average gained around 3%, and the Russell 2000 (small caps) advanced 4.3%. Our signature WealthTrust DBS Long Term Growth strategy has a current year-to-date performance gain of approximately 2.2% compared to the S&P 500 being flat.

The big catalyst came Wednesday: news of the ceasefire sent the S&P 500 soaring 2.5% in a single session—its strongest daily gain in a year. Industrials led the charge (+5.3% sector gain), benefiting from lower energy costs and renewed risk appetite. Consumer discretionary and technology also participated strongly, while energy stocks lagged as oil retreated.

By Friday, however, the mood turned choppier ahead of weekend diplomacy. The Dow fell 0.6% (about 269 points), the S&P 500 dipped 0.1%, and the Nasdaq eked out a modest 0.4% gain. Still, the weekly scoreboard was decisively positive, with the Dow briefly turning positive for the year at one point near 48,186 before closing around 47,917. The S&P 500 ended the week near 6,817.

This rebound follows a tough March and early April, when escalating conflict pushed the S&P 500 down roughly 4–5% year-to-date at its lows. The ceasefire provided a classic “relief rally,” rewarding sectors sensitive to energy prices and global trade while highlighting the market’s pent-up demand for de-escalation.

Bonds and Rates: Muted Reaction, Yields Edge Higher

Treasury yields showed remarkable restraint despite the equity rally. The 10-year Treasury yield ended the week around 4.31%, down only modestly on the week. The 2-year yield hovered near 3.81%.

The bond market’s subdued response reflects skepticism that the ceasefire will fundamentally alter the inflation or growth outlook quickly. Fed officials have signaled patience, with recent minutes and projections showing several members expecting zero rate cuts in 2026. Higher oil prices earlier in the conflict had already pushed markets to price out anticipated easing, and the temporary truce hasn’t reversed that fully.

Credit markets, however, brightened: high-yield spreads tightened to levels last seen in late January, signaling improving investor confidence in corporate balance sheets.

Commodities: Oil Plunges on Ceasefire Hopes

Oil was the week’s biggest mover. Brent and WTI crude fell sharply—oil dropped about 11% at one point—after the ceasefire news eased fears of prolonged disruption to the Strait of Hormuz, a critical chokepoint for global energy flows. Prices had spiked dramatically since late February amid the conflict, contributing to inflation concerns.

Gold, a traditional safe-haven, saw some profit-taking but remained elevated overall, reflecting lingering uncertainty. The dollar index slipped modestly as the risk appetite improved.

Economic Data: Inflation Jumps, Jobs Hold Steady

Friday’s March CPI report landed as expected but still stung, headline prices rose 0.9% month-over-month and 3.3% year-over-year—the highest annual pace since May 2024. Energy costs were the clear culprit, underscoring how geopolitical shocks can quickly feed consumer prices. Core CPI (excluding food and energy) was more contained.

On the jobs front, March nonfarm payrolls had shown resilience earlier (+178k, well above expectations), with the unemployment rate steady at 4.3%. This mixed picture—sticky inflation alongside a still-functional labor market—leaves the Federal Reserve in “wait-and-see” mode. No rate cuts are fully priced in for the rest of 2026, and the door to hikes remains theoretically open if inflation reaccelerates.

Q1 earnings season kicks off next week with major banks (JPMorgan, Goldman Sachs, etc.). Expectations remain for solid double-digit S&P 500 earnings growth overall, supported by resilient tech and energy sectors, though guidance could reflect caution around energy costs and consumer spending.

Geopolitics: Ceasefire Holds—for Now

The two-week truce is fragile and explicitly tied to reopening the Strait of Hormuz. Late-week reports suggested testing the agreement, with markets watching Saturday’s talks closely. A lasting de-escalation would be a major positive for global growth and inflation, benefiting energy-importing nations and reducing supply-chain pressures. Prolonged conflict, however, risks turning a short-term inflation spike into something more persistent.

Broader 2026 themes—AI investment cycles, tariff policy shifts, and defense spending—remain intact but are currently overshadowed by the Middle East drama.

Outlook: Cautious Optimism with Volatility Ahead

This week’s rally demonstrates markets’ eagerness for any sign of stabilization in the Middle East. Lower oil prices and reduced volatility (VIX dipping below 20) are tailwinds. Credit spreads tightening and small-caps outperforming suggest broadening participation beyond mega-cap tech.

Yet risks abound:

- The ceasefire is temporary—any breakdown could send oil and volatility spiking again.

- Inflation at 3.3% keeps the Fed sidelined, limiting monetary support.

- Earnings will need to be delivered to justify current valuations after the recent pullback.

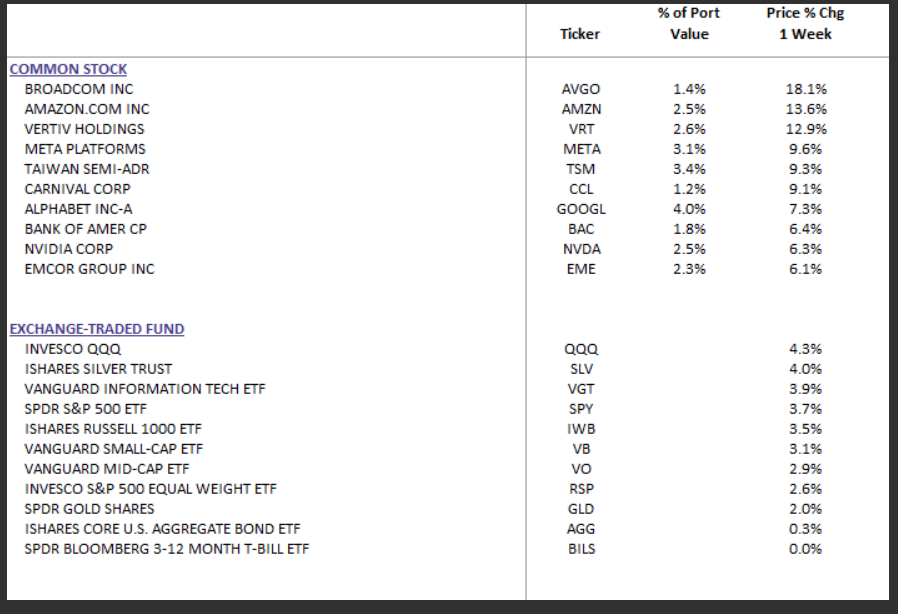

For investors, this environment rewards selectivity. Sectors less exposed to energy costs (technology, industrials in a recovery scenario) and those benefiting from lower input prices look attractive on dips. Defensive positioning in bonds or alternatives remains prudent, given uncertainty. We remain defensive with 20% of the portfolio in cash and short-term treasuries(BILS) in order to take advantage of the potential buying opportunities.

History shows geopolitical shocks often create buying opportunities once the immediate fear subsides—but only if the underlying economy and corporate earnings hold up. So far, they are.

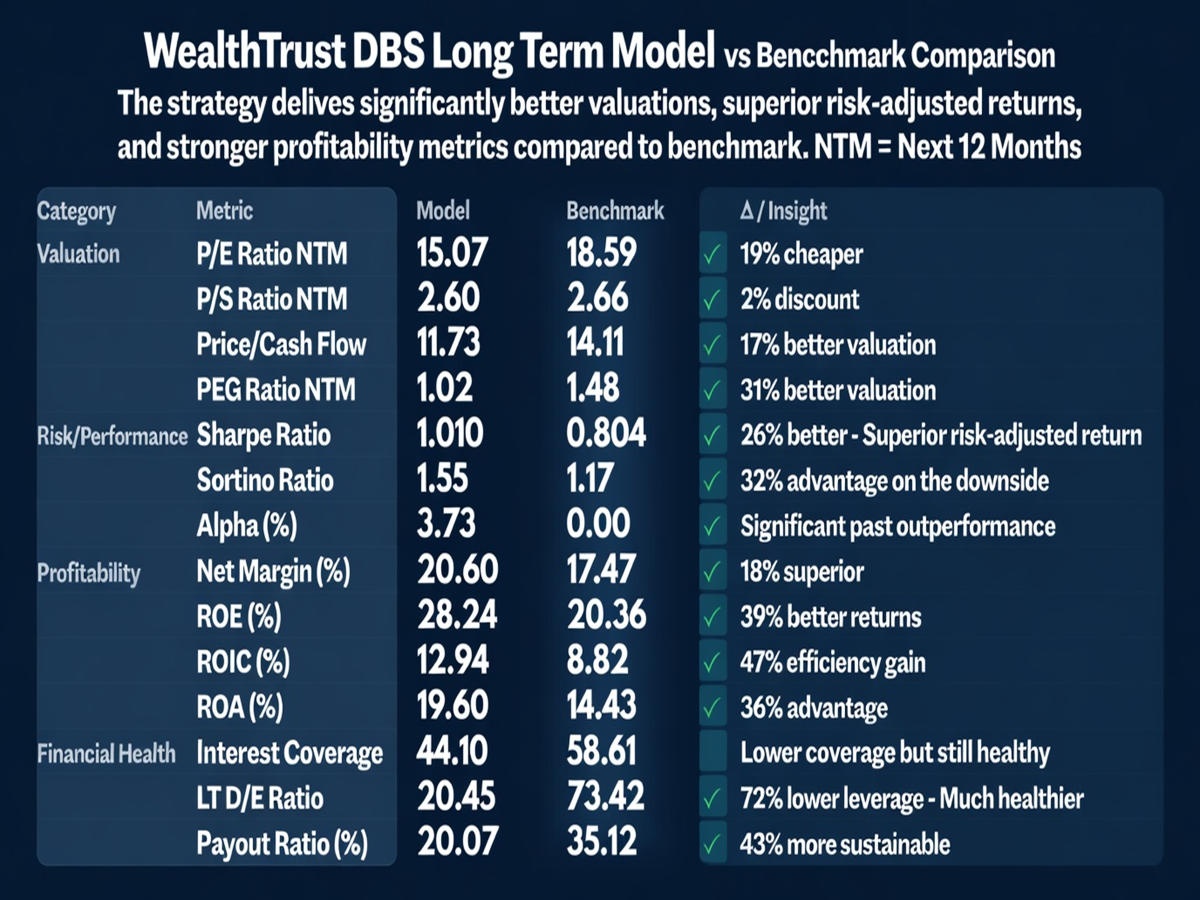

As you can see in the image below, our metrics are favorable in 13 of the 14 categories, especially our Next 12-month p/e ratio and peg ratio.

Bottom line: Markets celebrated the ceasefire this week, delivering the strongest gains in months. But with talks ongoing and inflation data reminding us of lingering pressures, this feels more like a truce in the market than a full resolution. Stay nimble, keep horizons long, and watch energy prices and weekend diplomacy closely—they’ll likely set the tone for next week.