Weekly Commentary for the week ending March 21, 2026

Welcome to this week's market update. Today we're reviewing a challenging period for investors as geopolitical risks, surging energy prices, and shifting monetary policy expectations combined to pressure equities. The major indices posted their fourth consecutive weekly decline—the first such streak for the Dow since 2023—amid persistent uncertainty surrounding the U.S.-Iran conflict and its ripple effects on inflation and growth.

Let's start with the numbers. For the week ending March 20:

- The S&P 500 fell approximately 2.1%, closing around 6,506.

- The Dow Jones Industrial Average dropped about 2.1%, ending near 45,577.

- The Nasdaq Composite declined roughly 2.1%, finishing at 21,648.

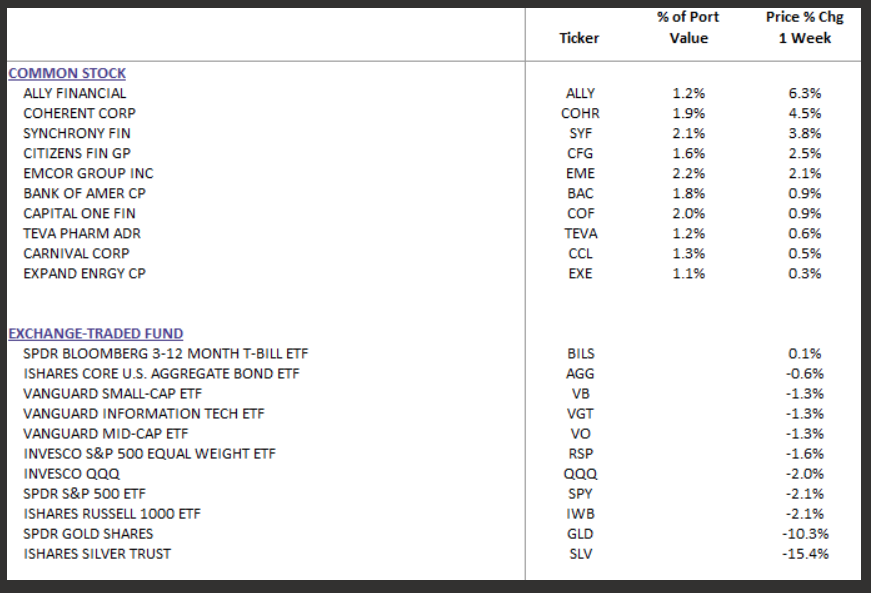

- Small caps underperformed sharply, with the Russell 2000 down over 2% on Friday alone, pushing it into correction territory (down more than 10% from recent highs). The Vanguard Small Cap and Mid Cap, both held within our DBS Long Term Growth Strategy were down 1.3% each, significantly outperforming the indexes.

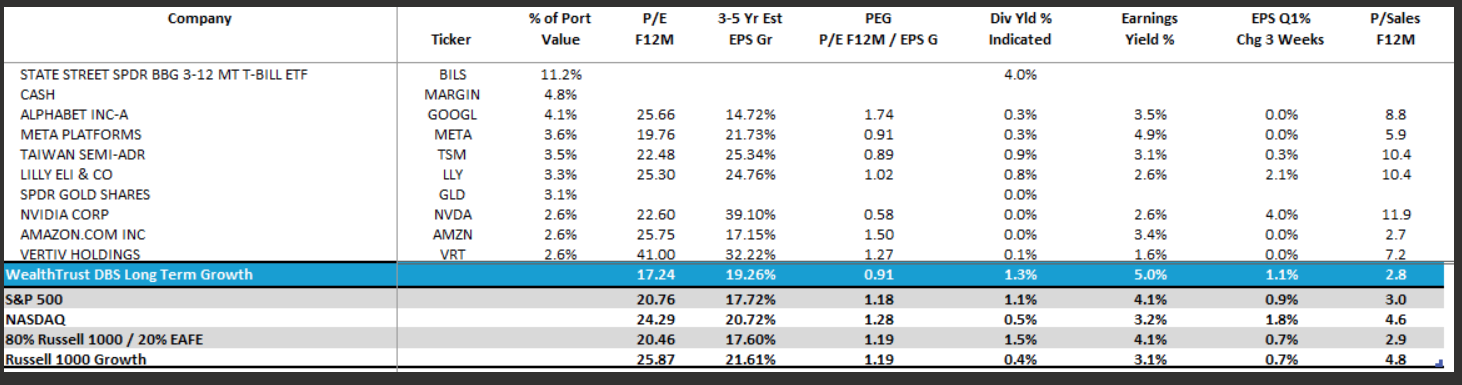

This downturn represents a continuation of the broad-based selling pressure that began in late February. Year-to-date, the S&P 500 is now down 4.68%, while the Dow Jones Large Cap Growth Index has declined 10.09%. In comparison, the WealthTrust DBS Long Term Growth Strategy is performing significantly better, with a more modest year-to-date loss of 2.68%.

Consistent with our earlier communications, we have meaningfully reduced exposure to higher-risk areas—most notably silver and technology—where the S&P 500 currently allocates 33.1% to technology, compared to our more defensive 22.8% weighting. We are maintaining approximately 16% in liquidity (primarily in Short Term Treasuries - BILS and Cash) to preserve flexibility and position us to deploy capital opportunistically as attractive entry points emerge.

Compared The dominant driver this week—and really the past several—was the escalation in the Middle East. The ongoing U.S.-Israel involvement against Iran has severely disrupted energy flows. Reports of halted tanker traffic through the Strait of Hormuz, force majeure declarations on key oilfields (including in Iraq), and strikes on major Gulf gas infrastructure sent crude prices sharply higher. WTI and Brent both pushed toward or above $100-$116 in intraday spikes at points, adding a significant risk premium.

Energy stocks were a bright spot, often the only positive sector, as higher oil bolstered producers like ExxonMobil. However, the broader market felt the pain: higher energy costs feed directly into inflation fears, squeezing consumer spending power and corporate margins in non-energy sectors.

This energy shock amplified concerns following the Federal Reserve's March meeting (concluded March 18). The FOMC voted 11-1 to hold the benchmark federal funds rate steady in the 3.50%-3.75% range. While that was widely expected, the updated Summary of Economic Projections (SEP) painted a more hawkish picture:

- Policymakers now forecast higher inflation for 2026, with core PCE expected around 2.7% (up from prior estimates).

- They still pencil in just one rate cut for the year, but Chair Powell emphasized "unusually high uncertainty" from the conflict. He noted that near-term energy-driven inflation could prove transitory if the situation resolves quickly—but no one knows the duration or scope. Rate hikes aren't off the table entirely if expectations unanchor, though that's seen as unlikely for now.

- Growth projections ticked slightly higher, but unemployment is expected to remain stable.

Markets interpreted this as a clear signal: fewer cuts (or none at all) in the near term, pushing out easing expectations well into 2027 in some pricing scenarios. Treasury yields rose accordingly—the 10-year climbed toward 4.38%—flattening the curve and adding pressure on rate-sensitive sectors like real estate, utilities (down over 4% Friday), and growth/tech names.

The Nasdaq felt this acutely, with AI-related and semiconductor stocks retreating amid broader risk-off flows. Names in tech hardware and data centers faced selling, while defensive rotation provided limited offset.

Other economic data points were mixed but overshadowed by geopolitics:

- Recent inflation readings (including hotter PPI) reinforced sticky services and energy components.

- Labor market signals softened modestly (February showed job losses in some reports), but not enough to override inflation worries.

- Consumer and business sentiment remains cautious, with volatility (VIX) elevated but not at panic levels.

Looking ahead, the path depends heavily on de-escalation in the Middle East. If diplomatic progress emerges or supply disruptions ease, we could see oil retreat and risk assets rebound history shows markets often shake off geopolitical shocks once the initial uncertainty fades.

Investor positioning thoughts:

- Maintain diversification.

- Cash and short-duration fixed income offer optionality if volatility persists.

- Long-term, fundamentals remain solid: corporate earnings resilience (outside energy-sensitive areas) and productivity tailwinds from tech/AI could support eventual recovery.

- Avoid overreacting to headlines; focus on duration of the energy shock and Fed signals.

In short, this drawdown stems more from external risks than a widespread economic breakdown. Markets are adjusting to persistently higher rates and energy volatility, yet strength in core sectors points to a contained—rather than systemic—selloff.

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

WealthTrust Long Term Growth Portfolio | Top 10 Equity Review