Weekly Commentary for the week ending March 7, 2026

Oil, Inflation, and Uncertainty: Markets Navigate a Shifting Landscape

Global markets experienced a volatile week as investors navigated a combination of rising geopolitical tensions, higher energy prices, and unexpected signs of economic weakness. The major U.S. equity indices finished the week lower as risk sentiment deteriorated. The S&P 500 declined roughly 1–2%, while the Dow Jones Industrial Average fell closer to 3%. The technology-heavy Nasdaq Composite was somewhat more resilient but still ended the week modestly lower. Small-cap stocks experienced heavier pressure, with the Russell 2000 dropping nearly 4% as investors moved away from economically sensitive segments of the market. Outside the United States, global equities also struggled. The MSCI Emerging Markets Index posted one of the weakest performances among major benchmarks as capital flowed into safer assets amid rising uncertainty.

The most significant catalyst for market volatility was the sharp move in energy prices. Oil markets surged as geopolitical tensions in the Middle East raised concerns about potential supply disruptions through the strategically critical Strait of Hormuz, a shipping route through which roughly one-fifth of the world’s oil supply passes. Prices for Brent Crude Oil climbed above $90 per barrel while West Texas Intermediate Crude Oil approached similar levels. This marked one of the strongest weekly increases in oil prices in several years and immediately raised concerns about the possibility of renewed inflation pressures. Higher energy prices tend to ripple throughout the global economy, increasing transportation costs, raising production expenses for manufacturers, and ultimately pushing consumer prices higher. As a result, energy stocks were among the few areas of the equity market that posted gains during the week, benefiting directly from the rise in commodity prices.

At the same time, economic data delivered an unwelcome surprise. The latest U.S. employment report showed that the economy unexpectedly lost jobs during the month, marking the first clear sign in several quarters that the labor market may be weakening. Payrolls declined by roughly ninety thousand jobs, and the unemployment rate edged up to approximately 4.4 percent. While a cooling labor market could normally encourage expectations for lower interest rates, the context of rising energy prices complicated the outlook. Investors now face the possibility that inflation could remain elevated even as economic growth slows. This combination of slowing growth and persistent inflation has revived concerns about stagflation, a scenario that historically presents significant challenges for policymakers and financial markets alike.

Bond markets reacted quickly to these developments. The yield on the benchmark U.S. 10-Year Treasury Note rose sharply during the week, climbing to around 4.1 percent. Rising yields reflect both inflation concerns and shifting expectations about the path of monetary policy. Higher Treasury yields also create headwinds for equities because they increase borrowing costs and make risk-free assets more attractive relative to stocks. Growth-oriented sectors such as technology and rate-sensitive industries like real estate and small-capitalization companies tend to feel the pressure most when interest rates move higher. Despite the rise in Treasury yields, credit markets remained relatively stable, suggesting that investors are currently more concerned about inflation risks than about a sharp deterioration in corporate credit conditions.

Sector performance across the equity market reflected these macro forces. Energy stocks led the market thanks to the surge in oil prices, while defensive sectors such as utilities and consumer staples held up relatively well as investors sought stability. Cyclical sectors more closely tied to economic growth—including industrials and financials—experienced greater weakness. Technology stocks delivered mixed results but showed relative resilience overall, supported by continued enthusiasm around long-term investment themes such as artificial intelligence. Large technology companies with strong balance sheets and dominant market positions continue to attract investor interest even during periods of broader market volatility.

International markets mirrored many of the same dynamics. European and Asian equities moved lower as investors reduced exposure to risk assets globally. Emerging markets faced additional pressure from a stronger U.S. dollar and higher energy prices. A rising dollar tends to tighten global financial conditions because many countries borrow in dollar-denominated debt, which becomes more expensive to service when the currency strengthens. For energy-importing emerging economies, higher oil prices also represent a direct drag on growth and trade balances, further contributing to market weakness.

Commodity markets were active beyond oil as well. Gold, traditionally viewed as a safe-haven asset during times of geopolitical tension, surprisingly declined slightly during the week. The pullback was largely attributed to the stronger U.S. dollar and profit-taking by investors following the metal’s strong performance earlier in the year. Currency markets reflected the shift toward safety, with the U.S. dollar strengthening against most major currencies as global investors moved toward dollar-denominated assets.

Digital assets also attracted attention during the week. Bitcoin rebounded strongly and climbed back above the $74,000 level after experiencing volatility earlier in the month. The recovery in the cryptocurrency market was partly driven by renewed optimism around regulatory clarity and increasing institutional interest in digital assets. While cryptocurrencies remain highly volatile, they continue to draw investor attention as an alternative asset class that can sometimes move independently of traditional markets.

Looking ahead, investors will closely monitor several key developments that could influence market direction in the coming weeks. Energy prices will remain a critical variable, particularly if geopolitical tensions escalate further or disrupt global supply chains. Continued increases in oil prices could reinforce inflation pressures and potentially delay expectations for interest rate cuts. At the same time, economic data will be scrutinized for signs that the labor market and broader economy are slowing more rapidly than anticipated. Housing data, consumer spending reports, and small-business sentiment indicators will provide additional insight into the health of the economy.

Monetary policy expectations will also remain in focus. Just a few weeks ago, markets were anticipating multiple interest rate cuts from the Federal Reserve this year. However, the combination of rising energy prices and lingering inflation concerns may complicate that outlook. Policymakers are likely to remain cautious until it becomes clearer whether the recent surge in oil prices represents a temporary geopolitical shock or a more persistent inflationary force.

Given this environment of uncertainty, maintaining portfolio flexibility becomes particularly valuable. At WealthTrust, maintaining approximately 15% of portfolios in liquid assets provides the ability to respond quickly as economic conditions evolve. Liquidity serves two important strategic purposes. First, it acts as a buffer during periods of market volatility, helping reduce overall portfolio risk when equities experience drawdowns. Second, it allows portfolios to be opportunistic. When markets pull back or when specific sectors become attractively valued, having liquid capital available allows investors to add to high-quality positions without needing to sell long-term holdings at unfavorable prices. In periods where the economic outlook may shift rapidly—whether due to inflation dynamics, interest rate changes, or geopolitical events—this liquidity provides the flexibility to rebalance, deploy capital into opportunities, or increase exposure to areas of the market that may benefit from the next phase of the cycle.

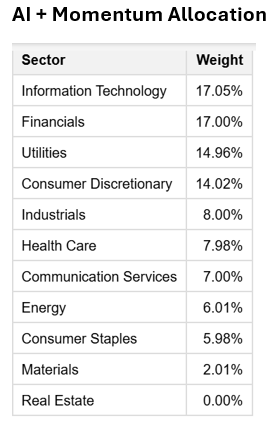

The AI + Momentum Sector Allocation strategy leverages artificial intelligence to dynamically optimize portfolio weights across U.S. equity sectors, combining predictive analytics with momentum signals to target outperforming areas while maintaining broad diversification. This AI-driven approach aims to enhance risk-adjusted returns by rotating toward high-momentum sectors amid evolving AI themes.

* A major key to outperformance is not only identifying sectors that are in favor but drilling down to identify the best companies to own within those sectors!

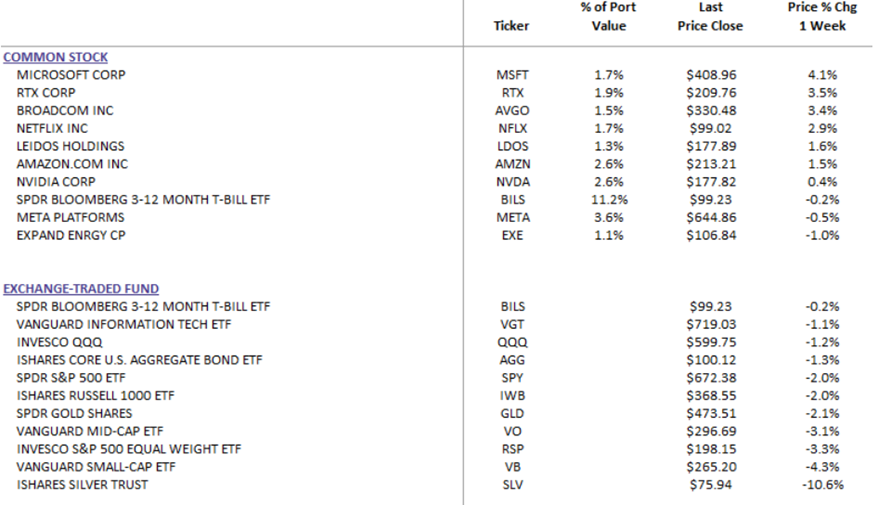

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

WealthTrust Long Term Growth Portfolio | Top 10 Equity Review

In summary, the week highlighted the delicate balance currently facing global markets. Rising oil prices, unexpected weakness in the labor market, and shifting interest rate expectations combined to create a challenging environment for risk assets. While long-term investment themes such as artificial intelligence and technological innovation continue to support certain sectors, near-term volatility is likely to persist as investors weigh geopolitical developments and incoming economic data. The central question for markets remains whether the global economy can slow enough to ease inflation pressures without tipping into a deeper downturn—a balance that will shape investor's sentiment and market performance in the months ahead. At the same time, maintaining liquidity and strategic flexibility positions investors to navigate these shifts while remaining prepared to capitalize on opportunities as they emerge.