Weekly Commentary for the week ending August 23, 2025

Weekly Market Commentary: Fed Signals Potential Rate Cuts Are On The Horizon

Market Overview

The U.S. equity markets displayed a mixed performance last week, with the S&P 500 Index rallying on Friday to close modestly higher after four days of losses. The rally was spurred by Federal Reserve Chair Jerome Powell’s remarks at the Jackson Hole symposium, which suggested that rate cuts may be on the horizon. Within the S&P 500, sectors such as energy, real estate, financials, and materials led the gains, while large-cap value stocks outperformed their growth counterparts. However, the Nasdaq Composite, heavily weighted in technology, ended the week lower, likely due to profit-taking and concerns over the sustainability of AI infrastructure spending.

The S&P Mid-Cap 400 and small-cap Russell 2000 indices posted strong returns, reflecting resilience in smaller companies. In the bond market, U.S. Treasuries rallied post-Powell’s speech, driving yields lower as bond prices rose.

Fed Chair Signals Potential Rate Cuts

In his Jackson Hole speech, Fed Chair Jerome Powell addressed the central bank’s dual mandate of controlling inflation and maximizing employment. He noted that the current federal funds rate (4.25%–4.5%) is restrictive and suggested that “downside risks to employment are rising” due to weaker labor demand and reduced labor supply from declining immigration. Powell’s comments signaled a potential shift in monetary policy, with a likely 0.25% rate cut in September and one to two additional cuts possible this year, followed by one to two in 2026. Markets reacted positively, with the probability of a September rate cut rising from 75% to 89%, per CME Fed Watch.

Powell also acknowledged near-term inflationary pressures, potentially driven by tariffs, but suggested these could be temporary. He described the labor market as being in a “curious balance,” with an unemployment rate of 4.2% but rising downside risks.

Economic Data: Manufacturing Surges, Labor Market Softens

The S&P Global U.S. PMI for August indicated robust business activity, with the composite PMI at 55.4, marking 31 consecutive months of expansion (above 50). The manufacturing PMI hit a 39-month high of 53.3, surpassing expectations of continued contraction, driven by rising demand and inventory buildup amid tariff-related supply concerns. However, the services PMI moderated slightly to 55.4 from 55.7.

Rising input costs, attributed to tariffs, led to the steepest increase in prices since May, with companies passing these costs to consumers. This aligns with Powell’s view of near-term inflation spikes that may stabilize if tariffs do not escalate further.

On the labor front, initial jobless claims rose to 235,000 for the week ending August 16, exceeding the Bloomberg consensus of 225,000. Continuing claims also increased to 1.972 million, signaling potential labor market softening.

Retail Earnings Highlight Consumer Resilience

Retail earnings provided a bright spot, with companies like Walmart, Home Depot, and Lowe’s reporting stronger-than-expected results. Amazon saw 11% growth in its North American retail sales for Q2. Retailers are navigating tariff-related cost increases by selectively raising prices on higher-margin products or absorbing costs on lower-ticket items. This resilience suggests consumers remain robust, though rising costs could pressure spending in the coming quarters.

Market Outlook and Opportunities

The S&P 500 has risen approximately 30% since its April 8 lows, but volatility may increase in the seasonally weaker months of September and October. Potential catalysts include rising inflation, softening economic data, and the upcoming U.S. tax bill, which could support corporate spending. Historical trends suggest two to three market pullbacks annually, which we view as opportunities to acquire quality investments at attractive prices.

We remain constructive on equities, favoring U.S. large- and mid-cap stocks for their diverse exposure across tech and non-tech sectors. Preferred sectors include technology, consumer discretionary, financials, and health care, which offer a balance of growth and value. In fixed income, bonds with 7- to 10-year maturities provide attractive yields and potential price appreciation if rates decline.

The Week Ahead

Key events include consumer spending data, PCE inflation, consumer confidence surveys, and NVIDIA’s Q2 earnings, which could influence market sentiment, particularly in the tech sector.

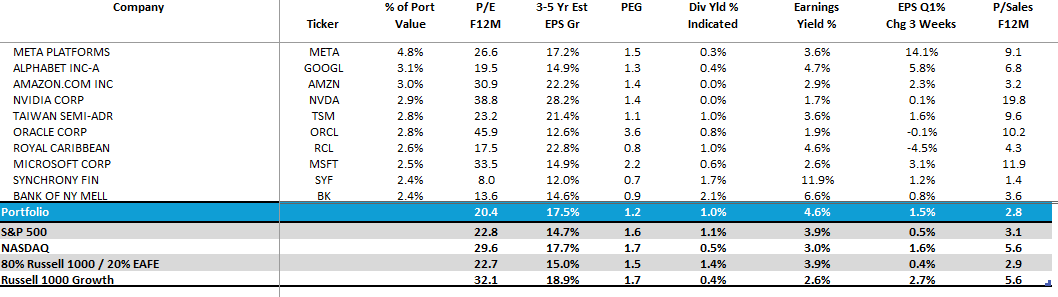

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

Top 10 Equity Review WealthTrust DBS Long Term Growth Portfolio