Weekly Market Commentary: Week Ending May 30, 2026

U.S. equities closed May 2026 on a strong note, with major indices setting fresh record highs in the final week. The S&P 500 finished near 7,580, the Dow Jones Industrial Average crossed 51,000 for the first time, and the Nasdaq Composite approached 27,000. A combination of de-escalating Middle East tensions (particularly U.S.-Iran ceasefire progress and potential Strait of Hormuz reopening), robust corporate earnings—especially in technology and AI-related sectors—and resilient U.S. economic data fueled the advance.

For the week ending May 29/30, the S&P 500 rose approximately 1.5%, the Nasdaq gained ~2.3%, the Dow added ~0.9%, and small-caps (Russell 2000) advanced ~1.7%. Monthly performance was solid, with the S&P 500 up around 6% (building on April’s stronger rebound), extending a multi-week winning streak amid optimism that geopolitical risks were peaking.

Volatility remained subdued (VIX down notably for the week), reflecting investor complacency and a “buy the dip” mentality focused on AI tailwinds over lingering macro uncertainties.

Weekly Recap (Week of May 25–30)

Markets built on prior momentum with a risk-on tone. Key drivers:

- Geopolitical Relief: Progress toward an extended U.S.-Iran ceasefire and reopening of the Strait of Hormuz eased supply concerns. Oil prices pulled back, reducing inflation fears and supporting equities.

- Tech and AI Leadership: Earnings from companies like Dell (up sharply on AI-server demand), Oracle, Salesforce, and broader semiconductor strength (e.g., Micron) propelled the Nasdaq. Cloud/AI themes dominated.

- Broad Participation: Small-caps and industrials joined the rally, though the Dow slightly lagged the Nasdaq on a relative basis.

Asian markets (e.g., Korea’s KOSPI) led globally at times, while Europe was more muted. Trading volume was steady but not euphoric, with decliners/advancers favoring bulls overall.

Monthly Performance (May 2026)

May consolidated April’s sharp rebound amid initial ceasefire optimism and strong Q1 earnings. The index extended gains modestly while hitting records, adding trillions in market cap since late March.

Sector Snapshot:

- Winners: Information Technology (AI infrastructure, semiconductors, cloud), Consumer Discretionary, Industrials, and Real Estate benefited from growth optimism and lower oil.

- Laggards: Energy faced pressure as oil retreated on peace hopes (though still elevated year-to-date). Health Care was mixed/weak.

International equities showed strength, with emerging markets (especially Asia) outperforming at points on tech exposure.

Macro and Economic Backdrop

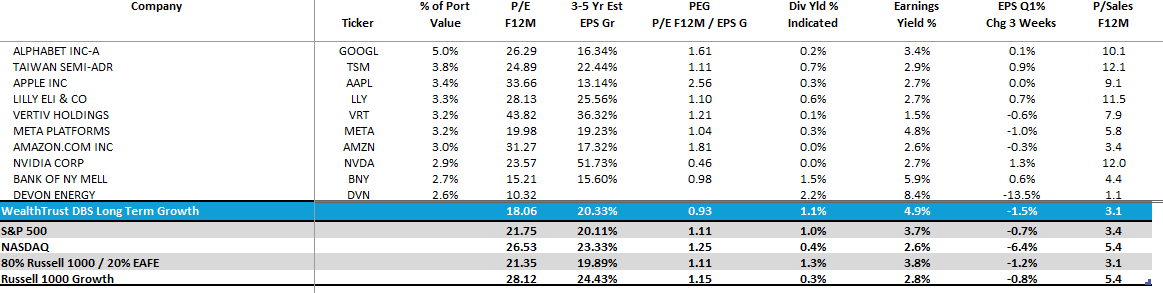

- Economy: Solid jobs data, retail sales, and corporate profits supported the narrative of a resilient “soft landing” or no-landing scenario. Q1 earnings beat rates were high (~84% positive EPS surprises), with AI driving margins. Historically this number is approximately 70% to 75% for the S&P 500 while WealthTrust's Quarterly beats are approximately 90% to 95% of the time.

- Inflation & Policy: Oil volatility (initial spikes from conflict, then declines) influenced expectations. Bond yields rose earlier in the period on higher-for-longer rate views but eased with oil. The Fed remained data-dependent, with speeches and minutes watched closely. No major rate moves, but cut expectations were tempered.

- Commodities:

- Oil (Brent/WTI): Volatile but trended lower toward month-end on ceasefire news (dropped to ~$87 in some reports). Still above pre-conflict levels overall.

- Gold: Mixed; supported by safe-haven flows early but capped by yields and dollar moves. Hit highs then pulled back.

- Bitcoin/Crypto: Under pressure from yields and risk rotation; pulled back from recent highs but remained relevant in broader risk asset discussions.

Key Themes and Risks

- AI as the Engine: Continued deployment and earnings validation have sustained the “Magnificent 7” and broader tech leadership. Productivity gains are real, but valuations and capex scrutiny could introduce volatility.

- Geopolitics: The U.S.-Iran dynamic remains fluid. Ceasefire extensions are positive, but any reversal could spike oil and yields again.

- Valuations and Sentiment: Records bring elevated multiples, especially in tech. Optimism is high (record S&P closes, low VIX), raising pullback risks around upcoming data (e.g., jobs, inflation). Small-caps lagged relatively at times, signaling selectivity.

- Bonds and Yields: Rebounded somewhat with oil relief, but higher-for-longer expectations persist, pressuring multiples.

Outlook

Markets have demonstrated remarkable resilience, shrugging off geopolitical shocks through earnings strength and thematic tailwinds. The broadening (small-caps, internationals) and record highs suggest underlying health, but the environment favors active selection over passive beta.

Bull Case: Sustained ceasefire, cooling oil, strong Q2 earnings, and AI momentum propel indices higher. Bear Case: Geopolitical flare-up, hotter inflation data, or Fed hawkishness triggers rotation out of growth.

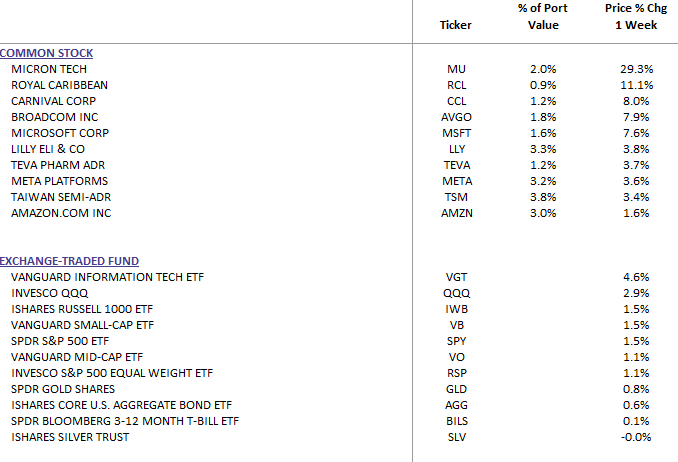

DBS Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

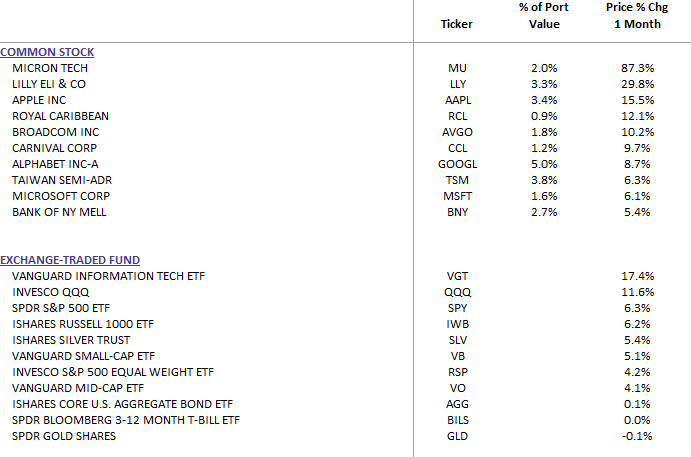

DBS Long-Term Growth Top Ten and Benchmark Monthly Performance Summary:

DBS Long Term Growth Portfolio | Top 10 Equity Review

Investors should maintain diversification, focus on quality earnings growth, and prepare for bumpier roads ahead. Position sizing around volatility events (economic releases, geopolitical headlines) remains prudent.