Weekly Market Commentary: Week Ending June 20, 2026

Markets demonstrated notable resilience this week, absorbing mid-week volatility before staging a strong rebound. The S&P 500 closed at approximately 7,501 on June 19 (up 1.08% that session), recovering from an intraday low near 7,402 earlier in the week. The Dow Jones Industrial Average continued its record-setting pace, trading near or above the 51,500 level with multiple fresh highs logged in recent sessions. The Nasdaq remained more volatile, reflecting swings in technology and semiconductor leadership, while the Russell 2000 showed pockets of relative strength, hinting at improving breadth.

Year-to-date, the S&P 500 has delivered solid mid-single-digit gains, with the Nasdaq outperforming on AI-driven momentum. This performance has occurred against a backdrop of elevated but manageable valuations, supported by robust earnings growth expectations (consensus forecasts remain in the high teens for 2026 in many sectors).

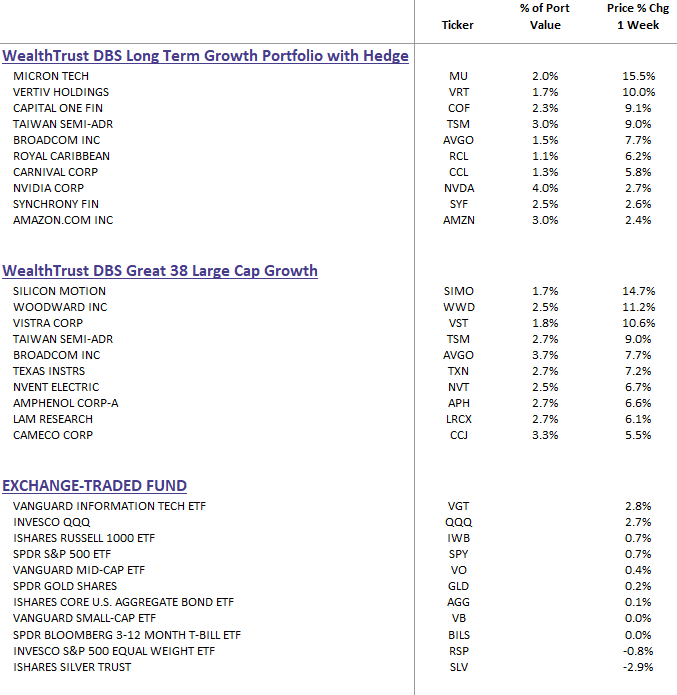

DBS Long-Term Growth & DBS Great 38 Large Cap Growth Top Ten and Benchmark Weekly Performance Summary:

For those interested in the WealthTrust DBS Great 38 Strategy, it is currently recommended as a stand alone strategy for new accounts of accredited investors with $1 million or more in liquid assets.

The strategy is also well-suited as a core/growth allocation by combining 50% in the DBS Long Term Growth Strategy (core) with 50% in the DBS Great 38 Strategy (growth) with a recommended investment of >$500k.

Geopolitical Relief Provides a Tailwind

The standout development was progress toward de-escalation in the Middle East. Reports of a U.S.-Iran framework agreement (or interim deal) to end hostilities, including steps toward reopening the Strait of Hormuz, triggered a sharp relief rally in risk assets and a meaningful drop in oil prices. Brent crude fell more than 5% at points, reaching three-month lows around the low-to-mid $70s before stabilizing.

This is a material positive. Lower energy prices ease input costs for businesses and consumers, reduce stagflationary pressures, and lower the risk premium that had been embedded in markets. Shipping normalization will take time, and U.S. fuel prices may remain elevated for months due to seasonal demand and logistics, but the directional shift in sentiment is clear. Geopolitical headlines that once weighed on confidence now appear to be transitioning from a headwind to a potential catalyst for broader participation.

That said, diplomacy remains fluid—markets are pricing in the positive scenario while remaining alert to any reversals. The reduction in tail risk has helped equities hold near all-time highs despite other crosscurrents.

Macro Backdrop: Sticky Inflation Meets Resilient Growth

Inflation data released this period showed the Consumer Price Index rising 4.2% year-over-year in May, above April’s 3.8% reading and in line with expectations but still elevated relative to the Fed’s target. This stickiness, combined with strong economic momentum and AI-related capital spending, has kept the Federal Reserve in focus. Market pricing and some Fed commentary have increased the perceived odds of a rate hike later this year (possibly by October), with the 10-year Treasury yield ending the week near 4.48%.

The U.S. economy continues to show underlying strength. Corporate balance sheets are healthy, labor markets remain resilient (albeit cooling gradually), and consumer spending has held up better than many feared. The combination of sticky inflation and solid growth creates a “higher for longer” policy environment that challenges valuation multiples in the short term but supports earnings power over the medium term.

Internationally, developed and emerging markets have participated in the rally, though U.S. large-cap leadership (particularly AI-related) remains pronounced. Global supply-chain normalization post-Hormuz tensions should provide additional support to manufacturing and trade-sensitive sectors.

Earnings, AI Momentum, and Market Breadth

The corporate earnings picture remains a bright spot. A high percentage of S&P 500 companies have beaten expectations, with particular strength in technology and companies tied to AI infrastructure buildout. Hyperscaler and data-center capex guidance continues to impress, with hundreds of billions in planned spending reinforcing the multi-year investment cycle.

Semiconductor and AI-related names experienced sharp swings—big gains followed by profit-taking or rotation—but the underlying demand thesis for chips, memory, networking, and power infrastructure appears durable. The successful SpaceX IPO debut earlier in the period also underscored investor appetite for high-conviction innovation themes.

Importantly, market breadth has shown intermittent improvement. While mega-cap technology continues to dominate headlines and index returns, financials, healthcare, and select industrial names have led the Dow on several sessions. Small-cap outperformance in certain weeks (Russell 2000 +3.9% in one recent stretch) suggests that easier financial conditions and domestic growth exposure are beginning to attract capital.

Valuations remain elevated relative to history, but they are better justified when viewed against expected earnings growth and the productivity tailwinds from AI adoption. Our quantitative screens continue to highlight companies with upward earnings revisions and positive momentum characteristics—key signals we monitor closely.

Portfolio Implications and Our Approach

In an environment defined by resilient growth, easing (but not eliminated) geopolitical risk, sticky inflation, and rapid technological change, we believe active management with disciplined processes adds meaningful value. Passive indexing captures beta effectively in strong bull markets but can struggle with concentration risk and the lack of explicit sell disciplines when fundamentals deteriorate.

Our proprietary framework—centered on earnings revision analysis, AI-augmented momentum screening, quantitative and fundamental research, and strict risk management—remains well-suited here. The Great 38 Core strategy and our Long Term Growth approach emphasize companies demonstrating fundamental improvement and sustainable competitive advantages, while maintaining diversification across sectors and styles. Blends incorporating tactical equity components allow us to respond to shifting leadership (for example, greater weight in financials or value-oriented names when rotation favors them).

We continue to favor a balanced posture: meaningful exposure to AI infrastructure and productivity beneficiaries, paired with high-quality companies outside pure technology that can compound through a higher-rate, normalizing-energy-cost world. Downside protection via sell rules and position sizing remains a core tenet—especially important as valuations sit near the upper end of historical ranges and policy uncertainty persists.

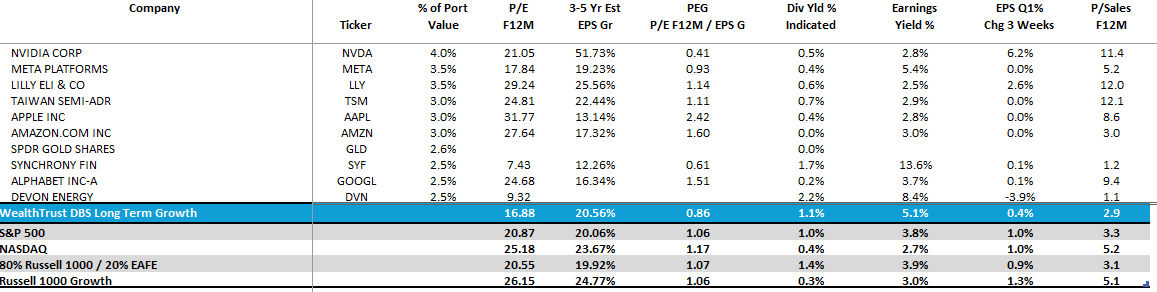

WealthTrust DBS Long Term Growth Portfolio | Top 10 Equity Review

Looking Ahead

The base case remains constructive for U.S. equities over the balance of 2026. AI-driven capital spending and productivity gains provide a powerful structural tailwind. Easing geopolitical tensions and lower energy prices remove a key source of volatility. Corporate earnings growth in the mid-to-high teens (or better in many cases) supports current price levels and offers room for multiple expansion or sustained outperformance if growth materializes as expected.

Risks are real and worth monitoring: persistent inflation could force a more hawkish Fed than markets currently anticipate; any diplomatic setbacks in the Middle East could reintroduce volatility; and rapid AI-related IPO supply later in the year may create technical headwinds. Valuations leave less margin for disappointment in high-expectation names.

We will continue to navigate these crosscurrents with the same numbers-first, process-driven discipline that has guided our strategies through prior cycles. Our focus remains on delivering consistent, risk-adjusted outcomes for clients while helping them sleep better at night through transparent communication and prudent portfolio construction.