Weekly Market Commentary - June 27, 2026

Markets exhibited notable volatility this week amid ongoing geopolitical developments in the Middle East, cooling oil prices, and mixed signals from the technology sector. The S&P 500 closed around 7,354 on Friday, reflecting a modest weekly pullback but remaining resilient near recent highs. The Nasdaq showed similar choppiness with tech/AI-related names under pressure, while broader indices like the Dow found relative stability.

This environment aligns with our proprietary quantitative framework, which emphasizes earnings revisions as a primary sell/buy signal. While headline indices faced headwinds, underlying fundamentals—particularly double-digit earnings growth expectations—continue to support a constructive outlook for disciplined active management.

Geopolitical Relief and Energy Markets

The dominant theme this week has been de-escalation signals following tensions involving Iran. Peace talks and diplomatic efforts appear to be progressing, with discussions around the Strait of Hormuz and regional stability gaining traction. Brent crude oil prices eased significantly, falling toward the low $70s per barrel by week's end from higher levels earlier in the period.

This reversal provided relief to consumers and businesses after earlier spikes that exacerbated inflation concerns. Lower energy costs are a tailwind for corporate margins and consumer spending, though we remain vigilant. Our models have long favored infrastructure and energy-adjacent plays with more durable characteristics over direct volatile commodity exposure. The pullback in oil underscores the importance of tactical sector rotation—shifting toward beneficiaries of normalized energy prices while maintaining hedges against renewed disruptions.

Earnings Momentum Remains the Bedrock

Despite market rotations, corporate earnings continue to deliver. Consensus expectations for S&P 500 EPS growth in 2026 hover in the low-to-mid 20% range, driven heavily by AI capital spending, resilient consumer demand, and operational efficiencies.

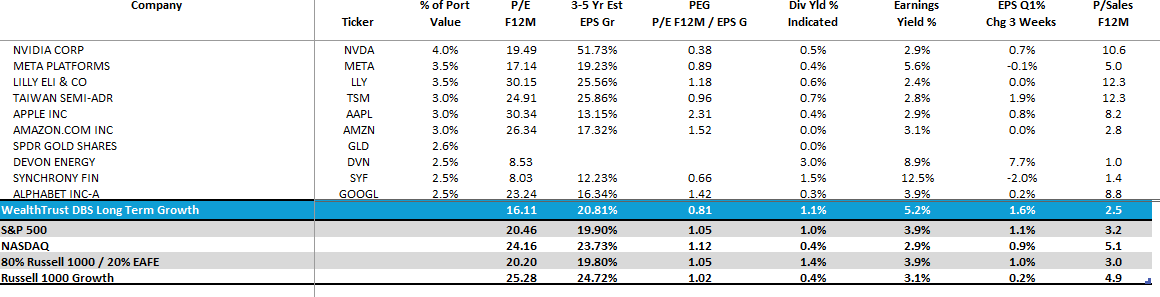

This week's reports (including key names like Micron and others in the semiconductor space) highlighted the dual nature of the AI trade: exceptional growth potential tempered by high valuations and the need for sustained execution. Earnings beats remain elevated, consistent with the strong Q1 trends carrying forward. Our "numbers first" approach—blending quantitative earnings revision signals with fundamental verification—continues to identify opportunities where upward revisions are broadening beyond the mega-caps (See the Weekly Performance Summary Below).

Valuations have moderated somewhat from peaks, with the S&P 500's forward P/E around 20x in recent readings. This provides a more reasonable entry point for high-quality growth names, especially those demonstrating strong momentum in our AI screening process. We continue to favor a hybrid model: concentrated core holdings verified through our three-fold process (AI-generated candidates, quantitative/fundamental review, and momentum confirmation).

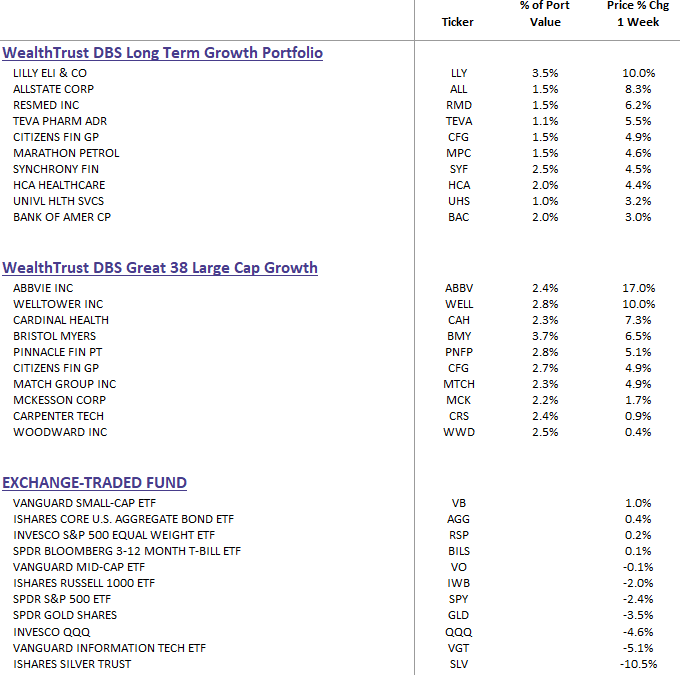

DBS Long-Term Growth & DBS Great 38 Large Cap Growth Top Ten and Benchmark Weekly Performance Summary:

Sector Rotation and Market Breadth

One of the healthiest developments has been signs of broadening participation. While technology and AI leaders faced profit-taking, areas like financials, industrials, and select "old economy" names showed relative strength. This rotation echoes patterns we've highlighted in prior commentaries—tech leadership persists but is complemented by cyclical recovery as geopolitical risks ease and rates stabilize.

The Russell 2000 and value-oriented segments have shown intermittent outperformance, suggesting improving breadth. Our Great 38 Core / Large Cap Growth strategy and WealthTrust DBS Long Term Growth approach are designed precisely for this environment: blending high-conviction growth with risk-managed diversification. Recent performance reviews (including 3-year 5-star Morningstar rankings for certain DBS strategies) affirm the value of this disciplined methodology, which has historically outperformed in approximately 75% of periods through earnings focus and sell discipline.

WealthTrust DBS Long Term Growth Portfolio | Top 10 Equity Review

Macro Backdrop: Inflation, Policy, and Consumer Resilience

Inflation data has been mixed but trending toward moderation as energy prices cool. The Federal Reserve's stance remains data-dependent, with markets pricing in potential rate adjustments later in the year. Resilient U.S. economic indicators—supported by strong corporate profits—provide a buffer against slowdown fears.

Consumer spending holds up, though we monitor for fatigue in lower-income cohorts. Multi-generational wealth planning remains front and center for our clients: strategies incorporating tax efficiency (e.g., capital loss harvesting, DSTs where appropriate) and diversified exposure help navigate uncertainty while positioning for long-term compounding.

Portfolio Implications and Risk Management

In our view, this is a market that rewards active oversight over passive indexing. Hidden concentration risks in a handful of mega-cap names, underscore the merits of our GIPS-verified strategies. We maintain tactical hedges, emphasize downside protection, and focus on companies with robust balance sheets and clear earnings trajectories.

For accredited investors, our 50/50 blends of Long-Term Growth with Great 38 Core continue to demonstrate strong risk-adjusted characteristics. Diversification across t(available on multiple TAMPs) or direct access remain key differentiators in our hybrid RIA model.

Looking Ahead As we head into the heart of summer, the interplay of easing geopolitical tensions, cooling energy prices, and robust corporate earnings sets a foundation for continued progress—albeit with volatility. Our quantitative models are flashing positive signals on net earnings revisions, supporting selective buying in pullbacks. However, elevated valuations in select growth pockets warrant caution; our sell rules are designed to protect capital when momentum fades.

We remain optimistic about America's innovative edge, particularly in AI and infrastructure, while prioritizing fiduciary standards and client outcomes. At WealthTrust, our goal is simple: deliver institutional-grade management so you can focus on what matters most—building and preserving multi-generational wealth while sleeping better at night.

For our current clients, thank you for the continued trust. We welcome conversations about how our strategies can integrate into your portfolios or partnership opportunities for RIAs and advisors seeking differentiated solutions.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Please consult your advisor for personalized guidance. Strategies are GIPS-verified; Morningstar ratings referenced where applicable.

This commentary is for informational purposes and reflects our views as of June 27, 2026. John G. McHugh, CPA, President & CIO, WealthTrust Asset Management LLC.