Weekly Market Commentary - July 11, 2026

Markets demonstrated notable resilience this week despite a flare-up in geopolitical tensions and the usual summer trading dynamics. Equities posted modest net gains, with the S&P 500 and Nasdaq Composite both advancing for a second consecutive week while the Dow Jones Industrial Average touched fresh all-time highs above 53,000 mid-period before settling with some giveback. The S&P 500 closed at 7,575.39, up approximately 1.4% for the week, while the Nasdaq rose about 1.7% to 26,281.61. The Dow ended near 52,637, down modestly on the week after its record-setting moves. Year-to-date, major benchmarks remain solidly in positive territory, with the S&P 500 up roughly 10.5% and the Nasdaq still showing double-digit gains.

Breadth showed some improvement relative to the narrow leadership seen earlier in the year, a development our quantitative models view constructively. Volatility remained contained overall, with the VIX hovering in the mid-teens, though intraday swings tied to headlines underscored the need for discipline.

Geopolitical Crosscurrents and Energy Market Volatility

The dominant macro story centered on renewed tensions in the Middle East. Early in the week, the U.S.-Iran ceasefire unraveled amid fresh strikes and rhetoric, raising concerns over the Strait of Hormuz and potential supply disruptions. Oil prices spiked sharply—rising as much as 7% intraday at one point—before easing as mediators stepped in, and some diplomatic language suggested pathways toward de-escalation. By week’s end, WTI crude settled near $72 and Brent around $76, still elevated from pre-conflict levels but well off the peaks seen earlier in the broader conflict.

This matters for inflation and growth. Energy remains a visible contributor to headline readings, and any sustained elevation adds to the stickier components of the price level. The Federal Reserve’s recent Monetary Policy Report highlighted inflation pressures from tariffs, Middle East factors, and surging demand for memory chips and semiconductors tied to AI infrastructure. Core measures have firmed, and markets are now pricing a higher probability that the Fed remains on hold at its late-July meeting, with the target range staying at 3.50%–3.75%. Minutes from the June FOMC revealed a divided committee, with some officials open to eventual cuts and others more hawkish given persistent price pressures. The next policy decision arrives July 28–29; upcoming data, particularly the June CPI release on July 14, will be closely watched.

For our process, the key is monitoring how these macro shifts translate into earnings revisions and sector leadership rather than reacting to every headline. Energy names that benefited from earlier spikes saw some profit-taking, while cost-sensitive areas found selective support on the oil pullback.

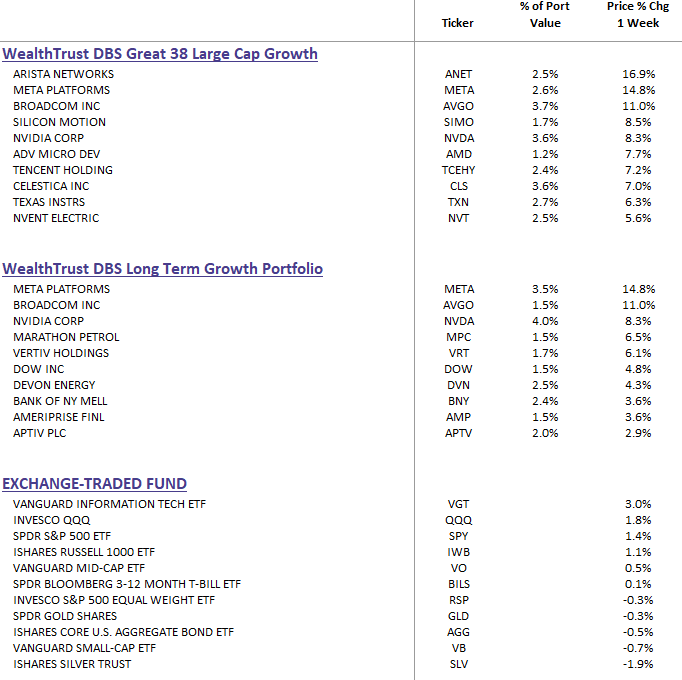

DBS Long-Term Growth & DBS Great 38 Large Cap Growth Top Ten and Benchmark Weekly Performance Summary

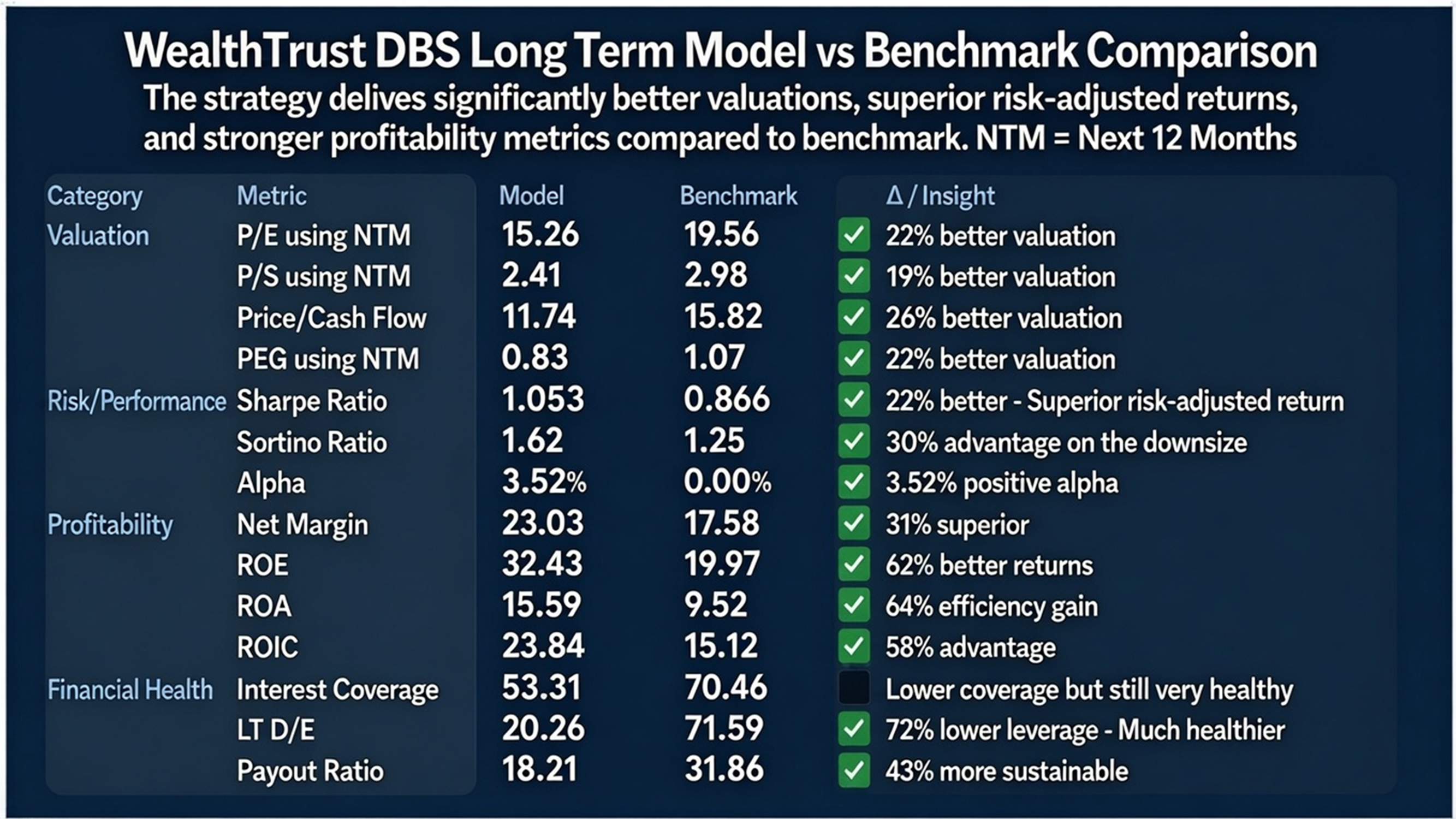

The WealthTrust DBS Long Term Model delivers significantly better valuations (e.g., 22% lower P/E), superior risk-adjusted returns (22% better Sharpe Ratio and 30% Sortino advantage), stronger profitability metrics (31% higher net margins, 62% better ROE), and a much healthier balance sheet versus the benchmark.

Corporate Earnings Momentum and the Broadening AI Cycle

Corporate America continues to deliver on the fundamentals that matter most. Forward earnings estimates for the S&P 500 remain robust, and Q2 reporting season begins in earnest next week with major banks (JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, and Goldman Sachs) kicking things off. Early indications suggest the AI monetization story that powered Q1 results is gaining further traction, with hyper scalers and key infrastructure players showing revenue acceleration in cloud and AI-related services.

The capital expenditure cycle shows no signs of meaningful deceleration. Investment is broadening beyond the initial hyper scaler surge into the physical layer—semiconductors, advanced packaging, cooling, power infrastructure, and related industrials. This is visible in order books, guidance, and sustained demand signals. Our AI momentum screening, layered with fundamental verification, continues to highlight companies where real monetization and earnings power are evident rather than narrative alone.

That said, the market has grown more discerning. Profit-taking in certain semiconductor names earlier in the period reflected classic digestion after an extended run rather than a fundamental breakdown. The rebound in chip stocks by week’s end reinforced that underlying demand remains intact, even as investors rotate toward names with clearer near-term visibility and more reasonable valuations. Our three-fold verification process—AI-generated candidates, quantitative and fundamental overlay, and momentum confirmation—has been particularly effective in navigating these rotations.

Quantitative Signals: Earnings Revisions Remain King

In environments defined by macro crosscurrents—geopolitics, inflation, Fed policy, and seasonal flows—earnings revisions continue to serve as our highest-conviction signal. Companies that consistently beat and raise estimates have historically outperformed, and our sell discipline, rooted in revision deterioration or momentum breakdown, provides a rules-based framework for risk management without abandoning the primary growth drivers.

We are also seeing early signs of improved market breadth. While mega-cap technology remains a powerful engine, participation from financials, select industrials, and other areas tied to the AI buildout has increased during relief moves. This aligns with our long-standing view that durable advances are rarely sustained by a narrow group of names. Valuation multiples have compressed modestly from earlier peaks; the S&P 500 forward P/E now sits closer to longer-term averages after the recent digestion. This creates a healthier setup for active management.

Risks Worth Monitoring

We remain vigilant on several fronts:

- Geopolitical re-escalation: Any reversal in Hormuz traffic, tanker incidents, or diplomatic progress could quickly reintroduce volatility and re-elevate the energy risk premium.

- Inflation persistence: Even with moderating oil, shelter, services, tariffs, and AI-driven chip demand could keep core readings elevated longer than hoped.

- Policy and data uncertainty: The June CPI print, bank earnings commentary on consumer and credit conditions, and the late-July FOMC will set the tone for the second half.

- Summer technicals: Lower volume periods can amplify moves in either direction; discipline around entry points and position sizing remains essential.

- Valuation pockets: Areas that ran hardest earlier in the year remain vulnerable to further mean-reversion if earnings delivery disappoints.

Positioning and the Path Forward

We continue to favor a balanced, active approach that combines secular growth exposure—via AI and technology leaders meeting our quantitative thresholds—with high-quality businesses showing broad earnings momentum across sectors. Blended allocations, such as meaningful exposure to the DBS Long Term Growth framework alongside the Great 38 Core strategy (or the Core/Growth Blend), goal is to deliver attractive risk-adjusted outcomes by reducing single-strategy concentration while maintaining a growth bias.

International and emerging markets participated selectively in recent moves, particularly where lower input costs or improving revision trends appear. We maintain exposure only where our models identify clear fundamental support and reasonable valuations.

The foundation of strong corporate earnings, ongoing AI-driven investment, and economic resilience gives us confidence that the longer-term trajectory remains upward—provided investors stay disciplined and avoid chasing or panicking at extremes. Markets do not move in straight lines. The recent volatility and subsequent recovery reinforce the value of a rules-based, numbers first process over reactive narratives.

Next week brings bank earnings, the critical CPI release, and continued monitoring of geopolitical and diplomatic developments. We expect volatility to persist but view the setup as constructive for selective, active management.

As always, I welcome your questions and look forward to speaking with you.

John, coming to you from Destin, Florida, President & Chief Investment Officer, WealthTrust Asset Management LLC

Additional details, including GIPS® verification information, are available upon request.

This commentary is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Please consult your financial advisor regarding your specific situation.