Weekly Commentary for the week ending May 16, 2026

Markets extended their winning streak to seven weeks, but the rally narrowed and faced fresh pressure by Friday. U.S. large-cap indexes, particularly those heavy in technology and AI, posted modest gains and touched fresh records mid-week. However, surging oil prices, climbing Treasury yields, hotter-than-expected inflation readings, and a lackluster Trump-Xi summit weighed on sentiment late in the period. Small-caps and international equities lagged noticeably.

U.S. Equity Markets: AI Optimism vs. Macro Pressures

The S&P 500 finished the week with a modest gain of roughly 0.2%, closing around 7,408–7,501 after setting intraday and closing records earlier. The index extended its streak despite a sharp pullback on Friday driven by higher yields and oil.

The Nasdaq 100 performed slightly better in relative terms early in the week but ended slightly negative (.35%) buoyed by AI-related strength. It also hit records mid-week.

Russell 2000 small caps underperformed sharply, declining around 2%, highlighting the narrow breadth of the rally. International stocks also lagged: MSCI EAFE (developed markets) and MSCI EM (emerging markets) posted notable weekly losses amid a stronger U.S. dollar and rising global rates.

Sector rotation was evident. Energy, healthcare, and consumer staples showed relative strength amid oil gains and defensive positioning. Technology benefited from AI enthusiasm, with standout moves in names like Cisco (strong earnings), NVIDIA, and the high-profile Cerebras Systems IPO, which soared post-debut after raising billions. Financials and industrials faced pressure from higher rates.

Corporate earnings continued to support sentiment. With a large portion of S&P 500 companies reporting Q1 results, earnings growth was robust (around 27%+ overall, with solid beats on revenue). AI infrastructure spending remained a key tailwind for big tech and related sectors, even as commentary noted mixed consumer trends (premium resilient, discretionary softer).

Fixed Income: Yields Spike on Inflation and Oil

Treasury yields rose sharply, reflecting inflation concerns and reduced expectations for near-term Fed easing. The 10-year U.S. Treasury yield climbed toward 4.5–4.6% (highest in over a year), while the 30-year pushed above 5.1%. This bond selloff pressured equities and other risk assets late in the week.

Higher yields stemmed from April CPI coming in at +3.8% YoY (a 3-year high) and PPI surging +6.0% YoY, both driven heavily by energy costs. Markets began pricing in a higher probability of Fed rate hikes (or delayed cuts) under incoming leadership. Mortgage rates also edged higher, with the 30-year fixed near 6.4–6.65%.

Commodities and Currencies

Oil was the dominant story, with WTI crude jumping sharply (up ~7.5% or more in the week, trading above $100–104/bbl at points) on ongoing Middle East tensions and disruptions in the Strait of Hormuz. This fueled inflation fears and supported energy stocks but acted as a broad headwind elsewhere.

Gold was mixed to softer, dipping amid the risk-off move and higher yields (which increase the opportunity cost of holding non-yielding assets). Silver saw more pronounced weakness. Bitcoin traded around $78,000–80,000, pulling back on the broader risk-asset pressure from yields and inflation repricing.

The U.S. dollar strengthened modestly, contributing to international equity underperformance.

Economic Data and Policy Backdrop

Key releases painted a mixed picture:

- Labor market showed resilience (e.g., nonfarm payrolls beating estimates earlier in the period).

- Inflation accelerated due to energy, with headline figures notably higher.

- Industrial production and other activity indicators remained solid, supported by business investment (especially AI/datacenters).

On the policy front, Jerome Powell's tenure as Fed Chair concluded around mid-May, with Kevin Warsh confirmed as successor. The Fed has held rates steady at 3.5–3.75%, acknowledging geopolitical risks. Markets are watching closely for signals from the new leadership on balancing inflation risks against growth.

Geopolitics remained central: the Trump-Xi summit delivered limited progress on trade, adding to uncertainty. Ongoing Middle East dynamics kept energy markets volatile.

Outlook: Resilience Tested

The U.S. economy demonstrates underlying strength—solid earnings, resilient consumer spending (especially higher-income), and AI-driven investment. However, persistent energy-driven inflation, higher borrowing costs, and geopolitical uncertainty introduce near-term risks. The rally's narrow leadership (concentrated in a handful of large-cap tech/AI names) suggests vulnerability if macro headwinds intensify.

Key factors to watch in the coming weeks:

- Further inflation and labor data.

- Progress (or lack thereof) on energy supply normalization.

- Corporate guidance on cost pressures and capex plans.

- Fed communications under new Chair Warsh.

Investors should maintain diversification. Quality large-caps with strong balance sheets and growth exposure have performed well, but broadening participation or a rotation into value/cyclicals could occur if inflation peaks and yields stabilize. Defensive positioning (e.g., energy, staples, or shorter-duration fixed income) may help navigate volatility.

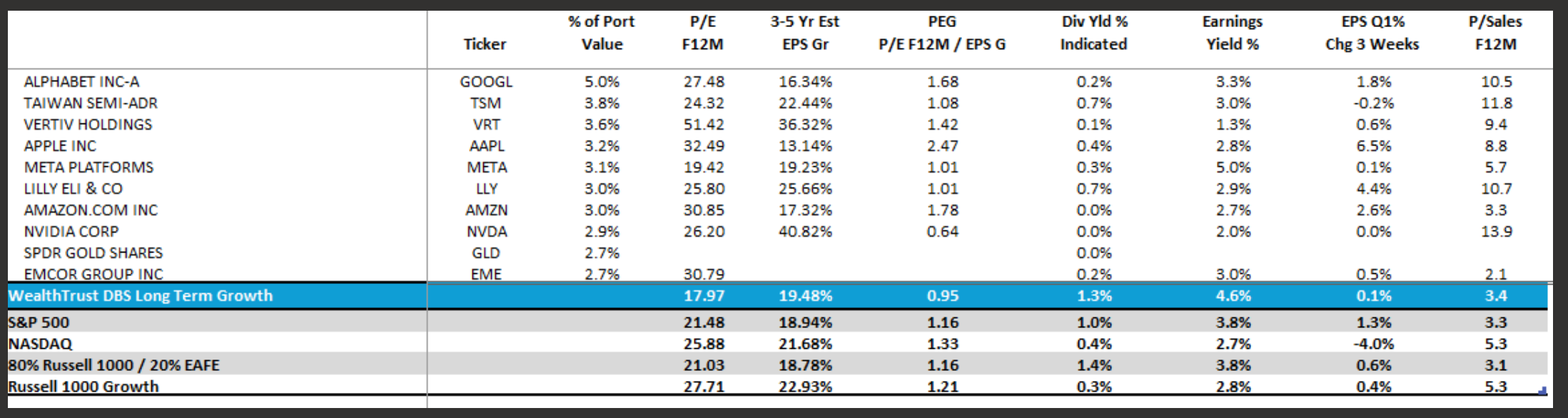

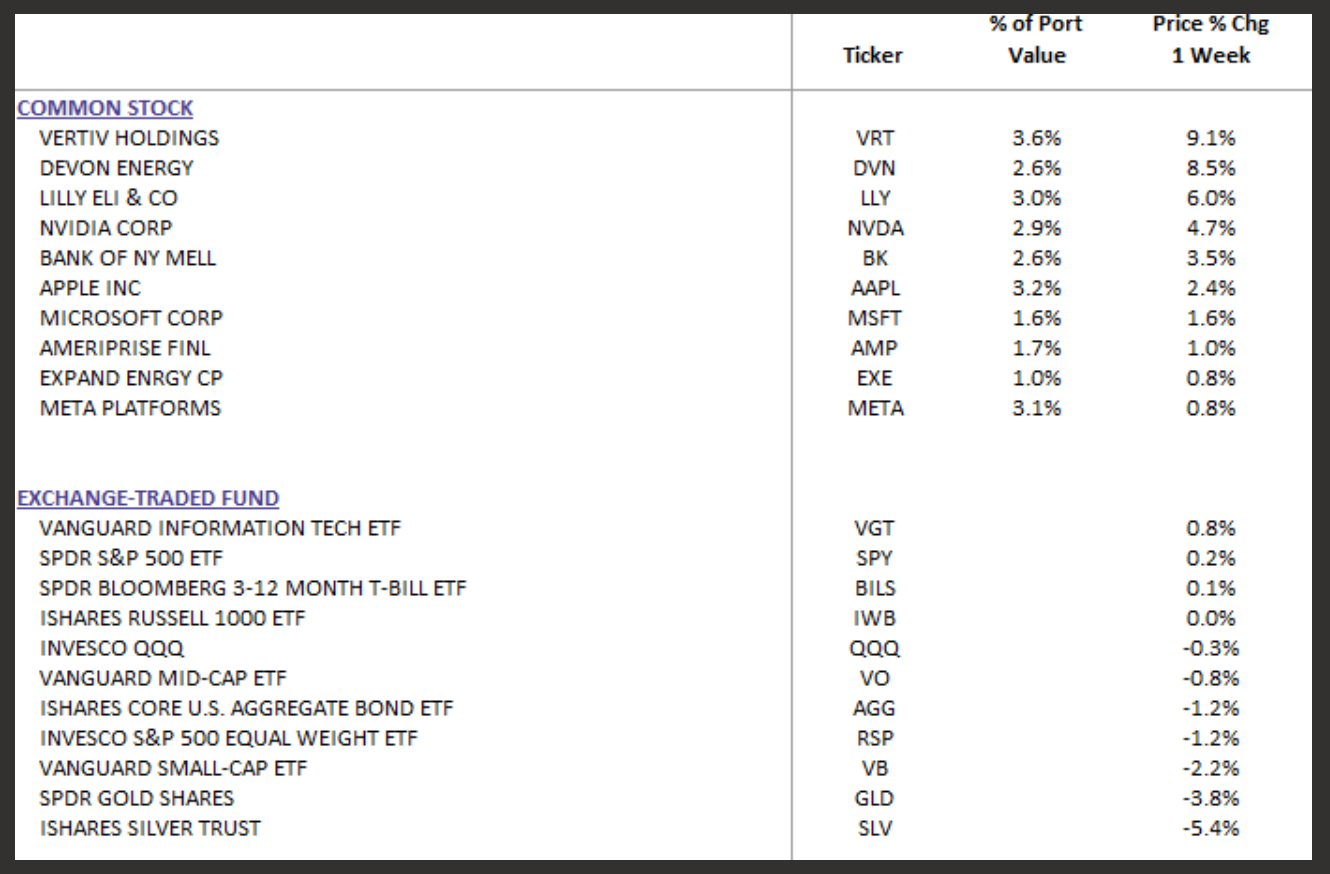

DBS Long-Term Growth Top Ten and Benchmark Weekly Performance Summary:

DBS Long Term Growth Portfolio | Top 10 Equity Review