Weekly Commentary for the week ending February 28, 2026

Financial markets were mixed in February as inflation continued to cool, economic growth remained steady, and corporate earnings stayed strong. Investors are increasingly optimistic that the economy can slow to a sustainable pace without falling into recession—a “soft landing.” While uncertainties remain, including interest rate timing, geopolitical tensions, and concentrated market leadership, the overall environment remains supportive for disciplined, diversified portfolios.

The U.S. economy continues to expand at a moderate pace. Consumer spending remains positive, though more measured, and the labor market is gradually cooling rather than weakening. Hiring has slowed modestly, job openings have declined, and wage growth is easing—an important factor helping inflation move lower. Price pressures continue to moderate as goods prices stabilize, housing costs ease, and services inflation begins to soften.

The Federal Reserve remains cautious. Interest rates are still restrictive, and the Fed continues reducing liquidity through quantitative tightening. Markets no longer expect rapid rate cuts; instead, they anticipate gradual easing later in 2026 if inflation continues to decline and growth remains stable. Financial conditions have stabilized in recent months, helping reduce rate volatility and support markets.

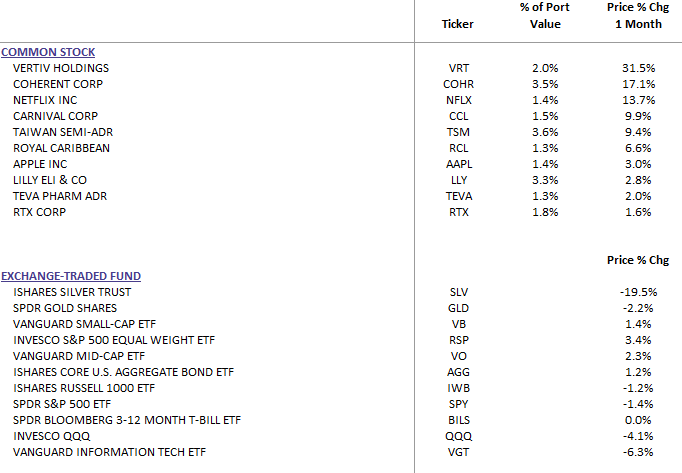

Stock markets were mixed during the month, although supported by strong earnings and continued business investment. Large technology companies and firms building artificial intelligence infrastructure remain key drivers of market performance. (See Taiwan Semi., Vertive Holdings, and Coherent Corp. performance below). Companies continue investing in automation and digital tools to improve productivity and offset labor costs. Market gains have also broadened modestly beyond the largest technology firms, with industrial and automation companies benefiting from infrastructure spending and supply chain reshoring. International stocks also advanced and may offer attractive valuations compared with U.S. markets.

Corporate earnings remain a major support for equities. Companies have maintained strong profit margins through pricing power, cost control, and efficiency gains from technology. Because markets expect earnings to remain strong, future performance will be sensitive to corporate guidance and earnings revisions.

Bond markets have stabilized as interest rate volatility declined. Yields have moved within a narrower range, and income is once again a meaningful contributor to bond returns. Credit markets remain healthy, supported by strong corporate balance sheets and low default rates. Investment-grade bonds continue to attract demand, while municipal bonds remain appealing for tax-efficient income.

Commodity markets showed mixed performance. Oil prices remain supported by supply constraints and geopolitical tensions. Industrial metals are benefiting from infrastructure spending and electrification trends. Gold and silver took some profit taking. Real assets—including infrastructure and energy transition investments—continue to provide diversification and potential inflation protection.

A notable development in credit markets is the rapid growth of private credit. Although private credit operates outside traditional bank balance sheets, banks remain deeply involved. They provide financing that allows private credit funds to make loans, offer hedging and structuring services, and often participate alongside private lenders in large deals. Private credit has taken market share in middle-market and leveraged lending, reducing banks’ direct loan growth and some fee income. Rather than being displaced, many banks have adapted by originating loans for private funds, forming joint lending platforms, and focusing on fee-based services while keeping risk off their balance sheets.

Despite its growth, private credit does not currently show the typical signs of a systemic credit bubble. Most loans are senior secured, negotiated privately, and give lenders strong control rights if borrowers face stress. Many funds require long investment lockups, reducing the risk of sudden investor withdrawals. While some aggressive lending practices and semi-liquid fund structures warrant monitoring, the market is diversified across industries and strategies. In an economic downturn, stress would more likely result in higher defaults, selective losses, and tighter lending conditions rather than a sudden market collapse. The relationship-driven structure of private credit suggests any repricing is more likely to be gradual than disorderly.

Key risks include policy missteps, geopolitical escalation, and the sustainability of earnings growth. Market leadership remains concentrated in large technology firms, which could increase volatility if sentiment shifts. Additionally, tighter lending conditions or rising defaults in private credit during a downturn could affect broader credit availability, though systemic risk currently appears limited.

From a portfolio perspective, maintaining exposure to high-quality companies with strong balance sheets and durable earnings remains prudent. Companies benefiting from automation, infrastructure investment, and productivity improvements may continue to perform well. Selective exposure to international markets may provide diversification and valuation advantages.

Within fixed income, emphasizing income through high-quality bonds and municipal securities remains appropriate. Balanced interest rate exposure can help manage uncertainty, while selective credit exposure may enhance yield. Real assets can provide diversification and inflation resilience.

Recent data continue to support the soft-landing narrative. Inflation readings have come in slightly below expectations, jobless claims remain low, and consumer activity is moderating but stable. Markets have responded positively to stable yields and constructive corporate guidance.

In the near term, markets may move within a range as investors assess economic data and the timing of policy changes. Over the intermediate term, earnings growth is expected to drive stock returns, while bonds provide income and diversification. Longer-term structural trends—including artificial intelligence-driven productivity gains, infrastructure investment, supply chain reshoring, private capital expansion, and demographic workforce changes—will continue shaping the investment landscape.

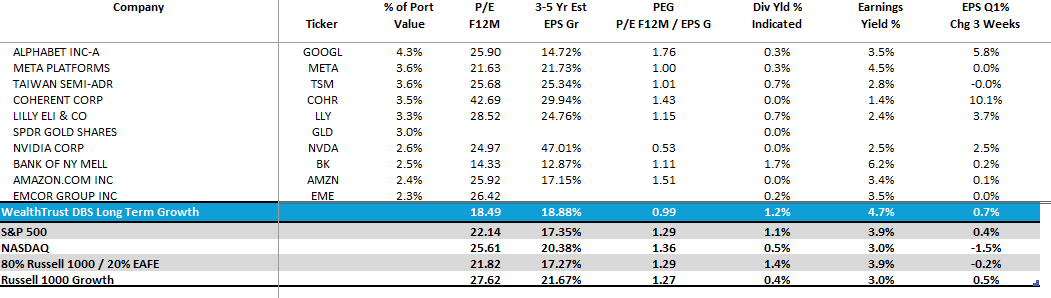

DBS Long Term Growth Top Ten and Benchmark Monthly Performance:

WealthTrust Long Term Growth Portfolio | Top 10 Equity Review

Overall, markets are navigating a transition defined by moderating inflation, steady growth, and evolving monetary policy. Stocks remain supported by earnings strength and productivity investment, while bonds once again provide meaningful income and stability. Maintaining diversification and focusing on long-term structural opportunities remain essential in the current environment.