Weekly Commentary for the week ending February 21, 2026

Good morning, everyone, and welcome to this week's market commentary for the week ending February 20, 2026. U.S. equities wrapped up a positive, holiday-shortened week on a note of relief, as markets digested the resolution of a key policy uncertainty.

The headline event was the U.S. Supreme Court's February 20 decision striking down the broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA), ruling that the president exceeded his authority in using the act to impose such measures. This overturned a significant portion of last year's tariff regime, which had generated notable revenue but introduced ongoing uncertainty for global trade, supply chains, and investor sentiment. The Supreme Court's recent decision to strike down IEEPA-based tariffs has had a limited overall impact on the broader U.S. economy, as the collected tariff revenues remain minimal compared to the economy's size and federal debt, with their inflationary effects contained so far and expected to diminish further. However, the ruling has removed a significant source of uncertainty for financial markets and investors, many of whom anticipated this outcome and expected the administration to pursue alternative tariff measures instead. The announced 10% tariffs align with existing rates and are unlikely to trigger major global trade disruptions or the panic seen in April 2025. As the administration conducts investigations over the next 150 days—coinciding with the U.S. midterm election season—Congress and voters may show limited appetite for significant tariff increases, potentially keeping future trade deals and rates more restrained. Overall, investors can breathe a sigh of relief that the decision aligned with expectations, and the administration's response remained predictable, while the tariff issue represents only a minor element of the macroeconomic landscape.

Markets responded positively to the reduced overhang: the S&P 500 rose about 0.7% on Friday to close at 6,909.51, posting a weekly gain of around 1.1%. The Nasdaq Composite snapped a five-week losing streak with a weekly advance of about 1.5%, closing higher on the day by 0.9%, while the Dow Jones Industrial Average added roughly 0.5% intraday to finish the week up modestly at about 0.3%. This bounce reflected eased fears of prolonged trade headwinds, even as the administration pivoted swiftly to new 10% global tariffs under alternative Trade Act authorities and initiated fresh Section 301 investigations.

The broader economic picture continues to support equities. January's jobs report showed nonfarm payrolls rising by 130,000—better than expected—with the unemployment rate edging down to 4.3%. Inflation readings have remained contained, and while recent GDP figures came in softer than anticipated (around 1.4% annualized for the prior quarter, impacted by temporary factors), overall U.S. economic growth is tracking near trend levels with resilient consumer and business activity bolstered by easing financial conditions and sustained AI-driven investments. Corporate earnings momentum remains a key tailwind, with analysts forecasting strong double-digit growth for the S&P 500 in 2026—projections ranging from around 12-14% overall, with some estimates as high as 14.7%, driven by broadening participation across sectors beyond the mega-caps. We've also seen positive signs of market breadth improving, with the current rotation toward cyclicals in recent sessions, even amid earlier AI-related concerns in big tech.

While the current rotation has created noise and downside, it's likely temporary—a natural balancing act after years of tech dominance. As midterm elections and trade probes unfold without major escalations, and with U.S. earnings on track for 13-15% growth, select AI stocks should return to the spotlight. Fundamentals like soaring AI spending ($2.5 trillion globally in 2026) and innovation cycles will outweigh short-term fears, drawing investors back. The key? Patience through volatility—stay diversified, but consider adding on weakness, as this setup mirrors past resets where AI leaders roared back stronger. If Nvidia's report next week delivers, it could kickstart the turnaround sooner than expected. While headlines around tariffs, geopolitics, and economic data can create noise, they haven't derailed the constructive fundamentals.

At WealthTrust, even though we are diversified, we believe that there will be a rotation back into technology once this rotation matures due to the sector's projected 30% earnings growth this year!

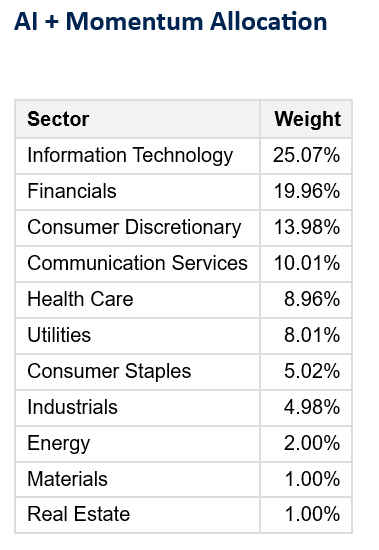

The AI + Momentum Sector Allocation strategy leverages artificial intelligence to dynamically optimize portfolio weights across U.S. equity sectors, combining predictive analytics with momentum signals to target outperforming areas while maintaining broad diversification. This AI-driven approach aims to enhance risk-adjusted returns by rotating toward high-momentum sectors amid evolving AI themes.

* A major key to outperformance is not only identifying sectors that are in favor but drilling down to identify the best companies to own within those sectors!

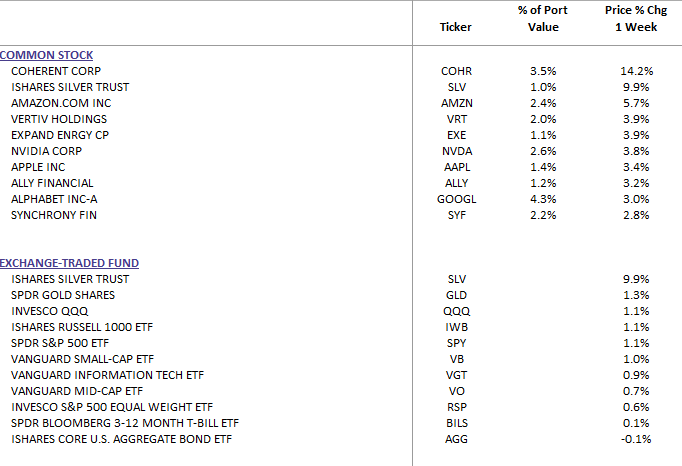

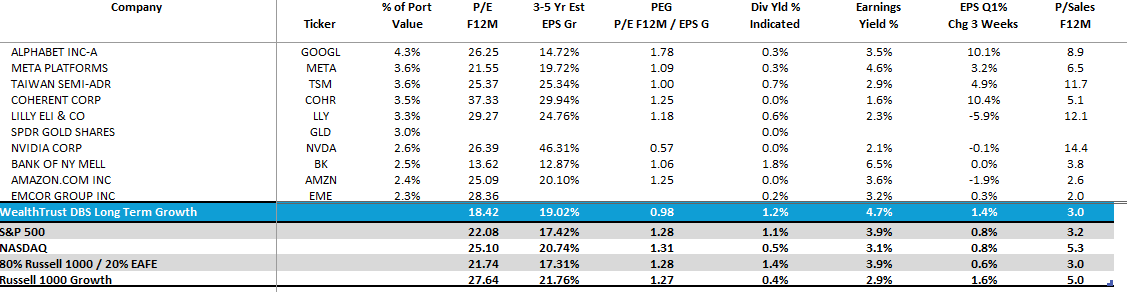

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

WealthTrust Long Term Growth Portfolio | Top 10 Equity Review

In summary, this week's Supreme Court ruling and measured market reaction represent a net positive by clearing one major uncertainty, reinforcing that—with solid U.S. growth, healthy corporate profits, and a still-supportive backdrop—the recommendation stands to stay diversified, remain invested through volatility, and tune out noisy headlines that do not meaningfully alter the bigger economic picture.