Weekly Commentary for the week ending February 14, 2026

Welcome to this week's market commentary for the week ending February 13, 2026. From my vantage point here in early 2026, we're reflecting on a volatile stretch that left many portfolios bruised but not broken.

The major indices wrapped up the week on a mixed note, with Friday offering only partial relief. The S&P 500 closed at 6,836.17, up a hair under 0.1% on the day but down 1.4% for the week overall. The Dow Jones Industrial Average settled at 49,500.93, gaining 0.1% Friday while posting a 1.2% weekly decline. The Nasdaq Composite, feeling the heaviest pressure, ended at 22,546.67—down 0.2% on Friday and 2.1% for the week. This represents the largest weekly drops of the year to date across the board, and the Nasdaq's fifth straight weekly loss has growth investors understandably on edge.

The catalyst for Friday's modest bounce came from the January CPI release, which delivered some welcome news on the inflation front. Inflation continues its slow grind lower. January data provided upbeat headlines, though price growth remains a bit too warm for full comfort just yet. Headline CPI rose 0.2% month-over-month—below expectations—pulling the year-over-year figure down to 2.4% from December's 2.7%. Lower energy prices played a key role in the slowdown, while core CPI (excluding food and energy) rose 0.3% m/m and landed at 2.5% y/y. This progress edges us closer to the Fed's 2% target and triggered a positive bond market response, with Treasury yields easing.

That said, a few considerations temper the enthusiasm. Some softness in the data may stem from the recent government shutdown, where the BLS imputed flat prices for missing October collections. More importantly, the Fed's preferred gauge—core PCE—is still forecast around 2.9% y/y for December, suggesting underlying pressures linger. On the brighter side, shelter inflation showed continued easing—a critical development, given how slowly housing costs filter into CPI due to BLS methodology. With house prices and rents having moderated in recent years, this trend should help pull overall inflation toward target over time, particularly as any lingering tariff-related effects dissipate.

Despite these encouraging macro signals—including a January jobs report that beat expectations on private-sector hiring—the broader market failed to mount a convincing recovery. The overriding theme? Renewed fears of AI-driven disruption spreading far beyond initial hotspots. What started with software-as-a-service concerns has now rippled into trucking, logistics, wealth management, insurance, office real estate, and even media sectors. This "AI angst" hammered high-valuation growth stocks, with the Magnificent Seven shedding more than 2% for the week and financials tumbling nearly 5%.

Yet not all was gloom. Defensive and traditional "old economy" pockets held firm or even gained ground—utilities, materials, real estate, consumer staples, and energy led the outperformers as money rotated toward names seen as more insulated from rapid AI upheaval. Market breadth told a nuanced story too: the equal-weighted S&P 500 outperformed its cap-weighted counterpart, highlighting how value and active stock selection are carving out edges in this environment of dispersion and style rotation.

Zooming out, U.S. stocks have been choppy without entering full capitulation mode. Many are framing this as healthy "chop" rather than outright "drop," with participants rotating sectors rather than fleeing equities. International and emerging markets outperformed domestically this week, offering a buffer for diversified portfolios. Commodities showed a split picture—energy softened, but gold climbed on safe-haven appeal.

Policy-wise, the Fed stays firmly in data-dependent territory. The target range for the federal funds rate holds at 3.5–3.75% after January's pause. With softer inflation prints in hand, markets now see about a 70% chance of rate cuts resuming by June, though March appears locked in as a hold. Resilient growth, cooling (but not collapsing) inflation, and a sturdy—if not scorching—labor market keep policymakers watchful rather than reactive.

Key takeaways for investors this week:

First, we're navigating a tug-of-war between solid fundamentals—easing inflation, robust job gains, steady expansion—and the profound uncertainties from technological change. Generative AI promises massive productivity gains but potentially challenges moats, spending patterns, and margins across industries.

Second, the rotation beneath the surface is constructive. Moving leadership from mega-cap tech to value, cyclicals, and defensives signals an evolving—not dying—bull market. This setup favors disciplined stock pickers over pure index exposure.

Third, expect continued volatility as earnings season unfolds, geopolitics simmers, and data flows in. The economy isn't flashing recession warnings, and supportive policy provides a backstop.

Note: At WealthTrust, even though we are diversified, we believe that there will be a rotation back into technology once this rotation matures due to the sector's projected 30% earnings growth this year!

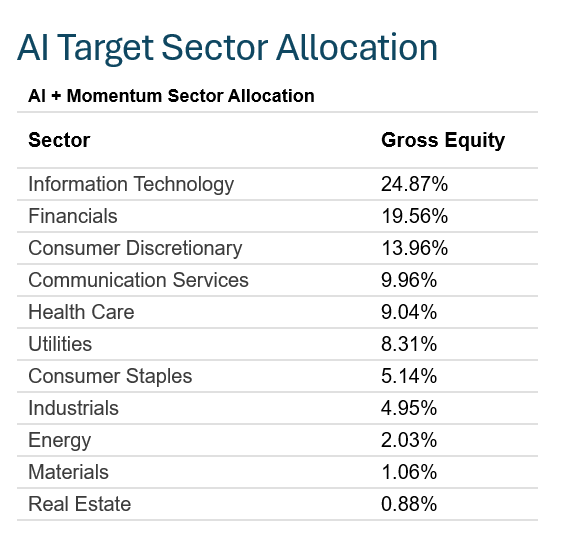

The AI + Momentum Sector Allocation strategy leverages artificial intelligence to dynamically optimize portfolio weights across U.S. equity sectors, combining predictive analytics with momentum signals to target outperforming areas while maintaining broad diversification. This AI-driven approach aims to enhance risk-adjusted returns by rotating toward high-momentum sectors amid evolving AI themes.

* A major key to outperformance is not only identifying sectors that are in favor but drilling down to identify the best companies to own within those sectors!

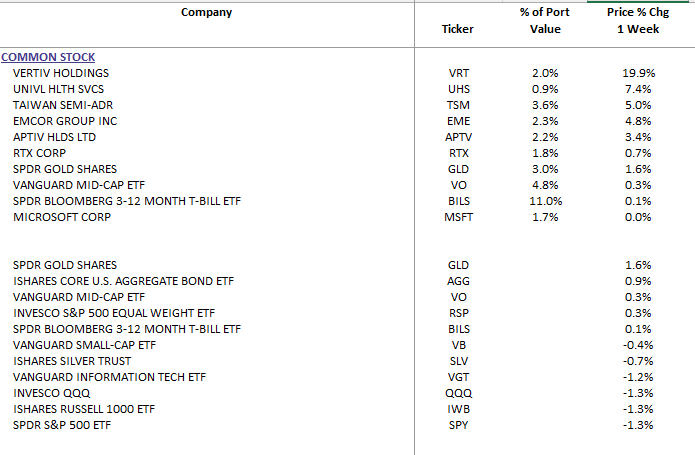

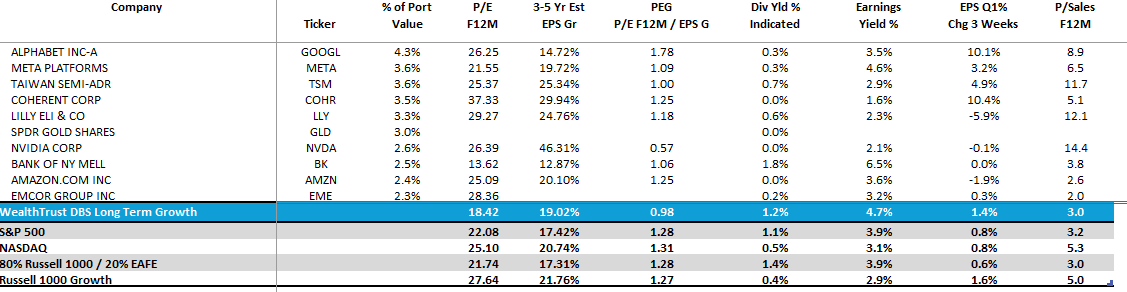

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

WealthTrust Long Term Growth Portfolio | Top 10 Equity Review

In closing, maintain diversification, hold a long-term view, and resist headline-driven moves. Markets seldom travel in straight lines; these periods of digestion frequently lay groundwork for the next advance—patience is the price of entry.