Weekly Commentary for the week ending April 3, 2026

Geopolitical Whiplash, Resilient Jobs Data, and a Volatile Rebound

The first week of April 2026 delivered another dose of headline-driven volatility, as markets swung between fears of prolonged conflict in the Middle East and tentative hopes for de-escalation. A surprisingly strong U.S. jobs report on Friday provided a counterweight to inflation worries fueled by surging oil prices, helping major U.S. indexes post solid weekly gains despite earlier turbulence. Investors navigated a complex mix of geopolitics, sticky inflation risks, and shifting Federal Reserve expectations—all while Good Friday closures thinned trading volumes in several major markets.

Equities: From Correction Fears to a Rebound

U.S. stocks staged a meaningful recovery amid fluctuating news from the Iran conflict. The S&P 500 rose about 3.4% for the week, closing near 6,583 after touching intraday lows earlier in the period. The Dow Jones Industrial Average added roughly 3%, while the tech-heavy Nasdaq Composite led with gains around 4%, benefiting from a relief rally in growth stocks as oil prices eased at times.

The week featured sharp intraday moves. On Tuesday (March 31), the Dow surged over 1,100 points and the S&P 500 jumped nearly 3%—its best day since May—on reports suggesting a possible near-term resolution to hostilities, including comments from President Trump about winding down U.S. involvement in 2–3 weeks. Oil prices pulling back temporarily fueled the risk-on sentiment. However, renewed rhetoric later in the week, including threats of escalated strikes, kept volatility elevated, with the VIX remaining in a nervous zone.

Smaller companies showed mixed resilience. The Russell 2000 gained ground on some sessions but remained sensitive to higher borrowing costs and energy expenses. Sector performance was uneven: Energy stocks faced pressure from volatile crude prices, while financials and consumer discretionary names benefited from the strong jobs backdrop. Technology and communication services outperformed on hopes that AI-related capex themes could endure beyond the immediate macro noise.

Internationally, the picture was more fragmented. European stocks rallied mid-week on de-escalation hopes, with the Stoxx Europe 600 and Germany's DAX posting gains of 2.7% in key sessions. Asian markets were volatile but ended with notable strength in spots—South Korea’s Kospi surged as much as 8% on strong export data and semiconductor demand, while Japan’s Nikkei rose on improved business sentiment. Emerging markets showed relative outperformance in patches, though energy-importing regions faced headwinds from higher oil costs. Overall, developed international equities lagged U.S. benchmarks on a monthly basis amid the broader risk environment.

Markets entered April still digesting a March selloff, with the S&P 500 flirting with correction territory (down ~10% from January highs at points) before rebounding. This marked yet another reminder that geopolitical shocks can accelerate drawdowns, even in an environment supported by underlying economic momentum.

Fixed Income: Yields Climb on Inflation Concerns

Treasury yields moved higher over the period as investors repriced the odds of Federal Reserve rate cuts. The 10-year U.S. Treasury yield hovered around 4.30–4.44%, up from earlier levels, while the 2-year note climbed toward 3.8–4.0%. The Bloomberg U.S. Aggregate Bond Index increased modestly, reflecting the inverse relationship between yields and prices.

The bond market’s reaction stemmed primarily from upside risks to inflation. Surging oil prices—driven by disruptions in the Strait of Hormuz and broader Middle East tensions—raised fears of a “stagflation-lite” scenario, where growth slows while prices accelerate. Earlier in March, markets had pushed back expected Fed easing, with some traders even pricing in a small chance of rate hikes later in 2026. The Fed itself kept rates steady in its prior meeting, emphasizing data dependence.

Corporate credit and high-yield spreads widened modestly at times but stabilized on the equity rebound. Municipal bonds and investment-grade corporates faced similar pressure from the higher-rate environment. For fixed-income investors, the environment remains challenging in the short term, though attractive yields provide a cushion compared to recent years.

Commodities: Oil Dominates the Narrative

Energy markets were the clearest story of the week. Oil prices (WTI and Brent) remained elevated and volatile, with Brent at times approaching or exceeding $100–$109 amid supply disruption fears. While prices eased on de-escalation headlines, the overall trajectory pointed to sustained upside risk. This marked one of the sharpest monthly surges in oil in decades, with March gains reported near 60% in some benchmarks.

Gold acted as a traditional safe haven, rising notably (up several percent weekly at points, with prices around $4,500–$4,675 per ounce before some pullbacks). It benefited from geopolitical uncertainty and inflation hedging demand, though it faced pressure when risk sentiment improved. Other commodities showed dispersion: Industrial metals were mixed, while agricultural prices reacted to broader macro flows.

Cryptocurrencies: Sideways Amid Macro Dominance

Bitcoin traded in a $65,000–$69,000 range, briefly testing higher levels before pulling back toward $66,000–$67,000. Ethereum and the broader crypto market followed a similar pattern, with modest recoveries interrupted by oil-driven selloffs. Crypto’s correlation with risk assets remained evident—gains on equity relief rallies gave way to weakness when headlines worsened or yields spiked. Market participants noted over $400 million in liquidations during sharp moves, underscoring the asset class’s sensitivity to leverage and sentiment. Bitcoin’s appeal as an inflation hedge has been tested in this higher-volatility regime, with traditional commodities like gold and oil stealing some attention.

Key Economic Data: Labor Market Surprise

The week culminated with a stronger-than-expected March jobs report released on Friday (April 3). U.S. employers added 178,000 nonfarm payroll jobs—nearly triple the consensus forecast of around 60,000. The unemployment rate dipped to 4.3% from 4.4%, and wage growth moderated slightly (average hourly earnings +0.2% month-over-month, +3.5% year-over-year).

This rebound came after a weak February (revised to a loss of 133,000 jobs, partly due to strikes and weather). The data suggested the labor market retains underlying resilience despite geopolitical uncertainty and prior softening. However, it also complicated the Fed’s task: Strong hiring reduces the urgency for rate cuts, while higher energy costs could keep inflation elevated.

Other indicators, including flash PMIs and import prices, pointed to ongoing economic expansion tempered by external shocks. Retail sales and upcoming inflation readings (CPI due soon) will provide further clarity on consumer health and price pressures.

Outlook: Caution with Selective Opportunities

Looking ahead, markets face several crosscurrents:

- Geopolitics remains the dominant wildcard. Any sustained de-escalation in the Middle East could ease oil prices, support risk assets, and allow central banks more breathing room. Conversely, prolonged disruptions would amplify inflation risks, pressure growth (especially in energy-importing regions), and keep volatility high.

- Fed policy path: With rate cuts now largely priced out for the near term (and some hike probabilities discussed), the central bank will watch incoming data closely. Sticky inflation from energy could delay easing, while any labor market softening might revive cut expectations.

- Earnings season begins in earnest soon, offering a window into corporate resilience. Sectors exposed to AI, defense, or domestic consumption may fare better than pure cyclicals sensitive to energy costs.

- Valuations and positioning: After recent drawdowns, some pockets of the market (particularly U.S. large-cap growth) look more reasonable, though overall multiples remain elevated by historical standards. Small caps and international equities could offer diversification if the U.S. dollar stabilizes or weakens.

For investors, this environment underscores the importance of discipline. Maintaining diversification across asset classes, focusing on high-quality companies with strong pricing power, and preserving liquidity to seize opportunistic opportunities remain prudent strategies.

History has shown that geopolitical “winters” are typically short-lived when compared to enduring structural growth trends. Continued advancements in AI adoption, productivity gains, and favorable demographic shifts in select economies continue to serve as powerful long-term tailwinds.

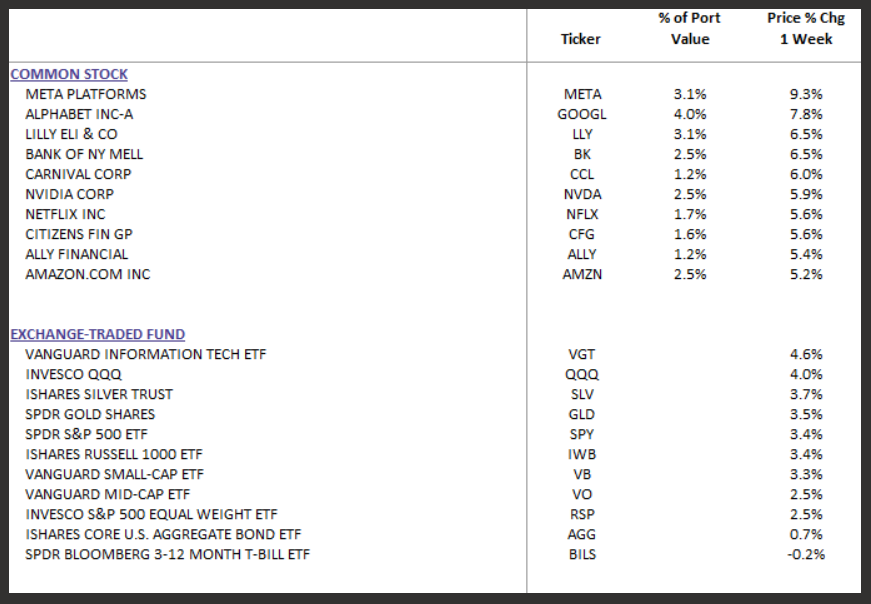

Consistent with this view maintain liquidity, as shown in the top 10 holdings report below, we have increased our allocation from 14% to 18% in short-term Treasuries(BILS).

The coming week will bring more inflation data, corporate earnings (including names like Delta Air Lines), and ongoing headlines from the Middle East and Washington. Expect continued two-way volatility, but also the potential for relief rallies if oil stabilizes or de-escalation signals strengthen.

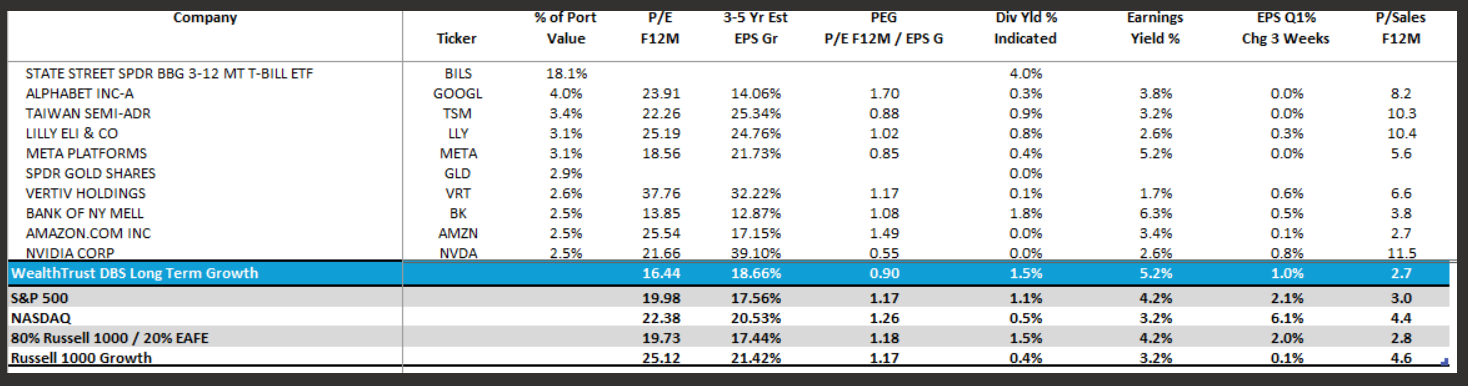

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

DBS Long Term Growth Portfolio | Top 10 Equity Review

In summary, the week underscored markets’ resilience amid uncertainty. A robust jobs' print and tactical rebounds offered encouragement, but higher-for-longer rates and energy-driven inflation risks keep the outlook guarded. Stay nimble, focus on fundamentals, and remember: In uncertain times, a balanced portfolio and a long-term horizon remain the most reliable guides.