Weekly Commentary for the week ending April 25, 2026

U.S. equity markets capped a strong week with fresh all-time highs, driven by de-escalating U.S.-Iran tensions, robust Q1 earnings (especially in tech), and resilient economic data. The S&P 500 climbed toward or above the 7,100–7,165 level, the Nasdaq led with tech strength, and the Dow showed more modest gains. Investors shrugged off lingering geopolitical risks as optimism grew around a potential longer-term ceasefire and reopened Strait of Hormuz traffic.

Key themes this week:

- Geopolitical relief outweighed war-related volatility.

- Earnings momentum supported valuations, with upward EPS revisions.

- Sector rotation favored tech/AI beneficiaries and cyclicals over defensives.

- Rates and commodities reflected mixed signals: yields stable-to-lower, oil volatile but off peaks.

Market Performance Snapshot

Major U.S. indices posted solid weekly gains amid record-setting closes mid-week.

- S&P 500: Closed the week near 7,158–7,165 (up ~0.8% on Friday alone in some reports), breaching 7,000 and setting new highs. Year-to-date, it recovered strongly into positive territory (~4%+).

- Nasdaq Composite: Outperformed with ~1.6% gains on strong days, hitting records around 24,800+. Tech leadership was evident.

- Dow Jones Industrial Average: More muted, hovering near 49,200–49,400, with gains of ~3% in prior weeks but steadier this period.

International markets (e.g., MSCI EAFE) also advanced on risk-on sentiment, though U.S. indices led.

Intraday/Weekly Volatility: Early-week dips on renewed tensions gave way to sharp rebounds on ceasefire hopes and oil pullbacks. The S&P 500 rallied over 12% from late-March lows in a rapid recovery.

Drivers of the Rally

- Geopolitical De-escalation: Optimism around U.S.-Iran ceasefire extensions and reopened shipping lanes through the Strait of Hormuz fueled the "risk-on" shift. Oil prices eased from spikes (trading ~$95–$103/barrel range, down from war peaks), reducing inflation fears. Markets had priced in significant disruption earlier; relief provided a tailwind.

- Strong Corporate Earnings: Q1 2026 earnings season delivered, with S&P 500 EPS growth projected at ~13–14% YoY—the sixth straight double-digit quarter. Tech led (semis up massively), financials beat on resilient banking activity, and upward revisions in 2026 estimates (~4% in some reports) boosted sentiment.

- Macro Backdrop: Mixed but supportive data. Consumer spending held up; GDP growth projections for 2026 remained around 2–2.5%. Unemployment is steady, nearly 4.3%. However, consumer confidence dipped, and war-related energy shocks added uncertainty.

Standouts included Intel (strong AI-related beat and outlook), banks like Goldman Sachs and JPMorgan, and AI supply-chain names.

Sector and Thematic Highlights

- Technology & AI: Clear winners. Nasdaq outperformance driven by AI optimism. Semiconductors and related hardware surged on demand signals. Intel's move highlighted broadening AI infrastructure needs beyond hyperscalers.

- Energy: Volatile. Oil prices swung on Hormuz news but eased overall, pressuring some names while benefiting refiners.

- Financials: Solid earnings but cautious guidance on macro risks.

- Defensives (Utilities, Staples, Healthcare): Lagged in the risk-on environment.

- Small-Caps: Benefited from rotation and lower-rate expectations longer-term.

Commodities:

- Oil: Volatile but lower on ceasefire hopes (~$95–$100 WTI range recently).

- Gold: Acted as a hedge but stabilized with dollar and oil moves.

- Bitcoin/Crypto: Mixed; gained on risk appetite but faced pressure from energy costs and macro.

Fixed Income: Treasury yields eased modestly. 10-year around 4.30–4.31% (down slightly week-over-week). Curve stable; Fed expected to hold rates at 3.50–3.75% into late 2026 amid inflation risks.

Risks and Outlook

Bull Case: Sustained ceasefire, strong earnings continuation (tech/AI super cycle), and soft-landing support further upside. S&P 500 could test higher records if inflation moderates.

Bear Case: Renewed Middle East flare-ups, sticky inflation from energy, or Fed hawkishness could trigger pullbacks. Valuations remain elevated; any earnings miss in coming weeks would matter.

Neutral/Base: Choppy but upward bias into summer, with focus shifting to Q2 earnings, Fed meeting (April 28–29, hold expected), and inflation prints. Earnings growth and AI themes provide a floor.

Investor sentiment has improved rapidly, but geopolitical residuals and policy uncertainty warrant caution. Diversification across sectors, quality earnings growers, and some defensive positioning remain prudent.

Key Takeaways for Investors

- Invested but selective: Favor companies with strong balance sheets, pricing power, and secular tailwinds (AI, productivity).

- Monitor geopolitics and oil closely—they remain swing factors.

- Portfolio balance: Equities for growth, fixed income for ballast, alternatives (e.g., gold) for hedge.

Longer-term: U.S. economy's resilience and corporate innovation continue to underpin markets despite headline risks.

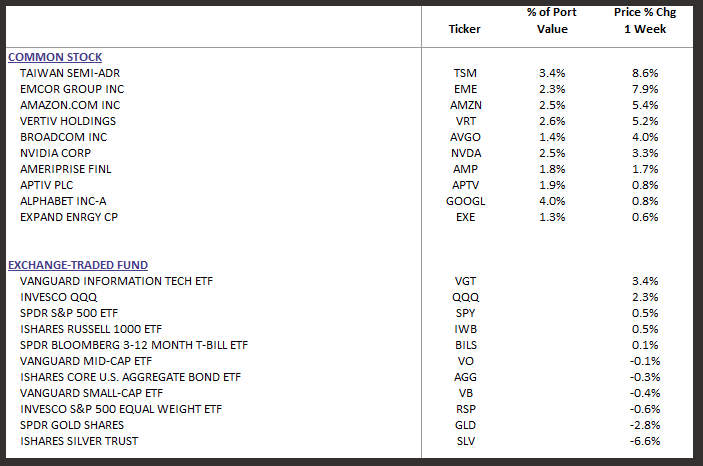

DBS Long Term Growth Top Ten and Benchmark Weekly Performance:

The WealthTrust DBS Long Term Growth Strategy's performance is in the top 2% in the Morningstar's Large Cap Blend Category on a risk adjusted basis.

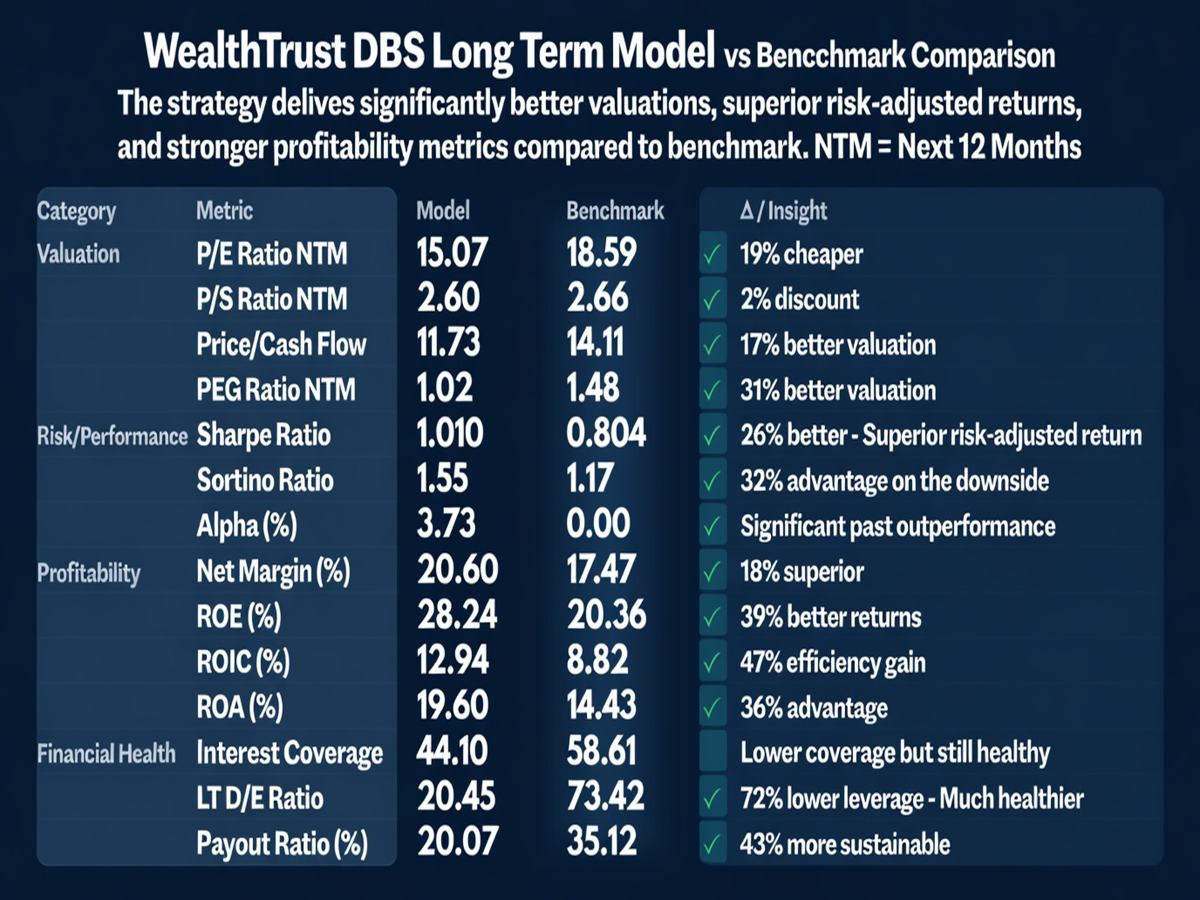

Past performance is no guarantee of future performance. Please see the image below.

The image below is as of 3-31-26 and as you can see, our metrics are favorable in 13 of the 14 categories, especially our Next 12-month P/E ratio and PEG ratio (p/e divided by the next 3–5-year earnings growth projection).

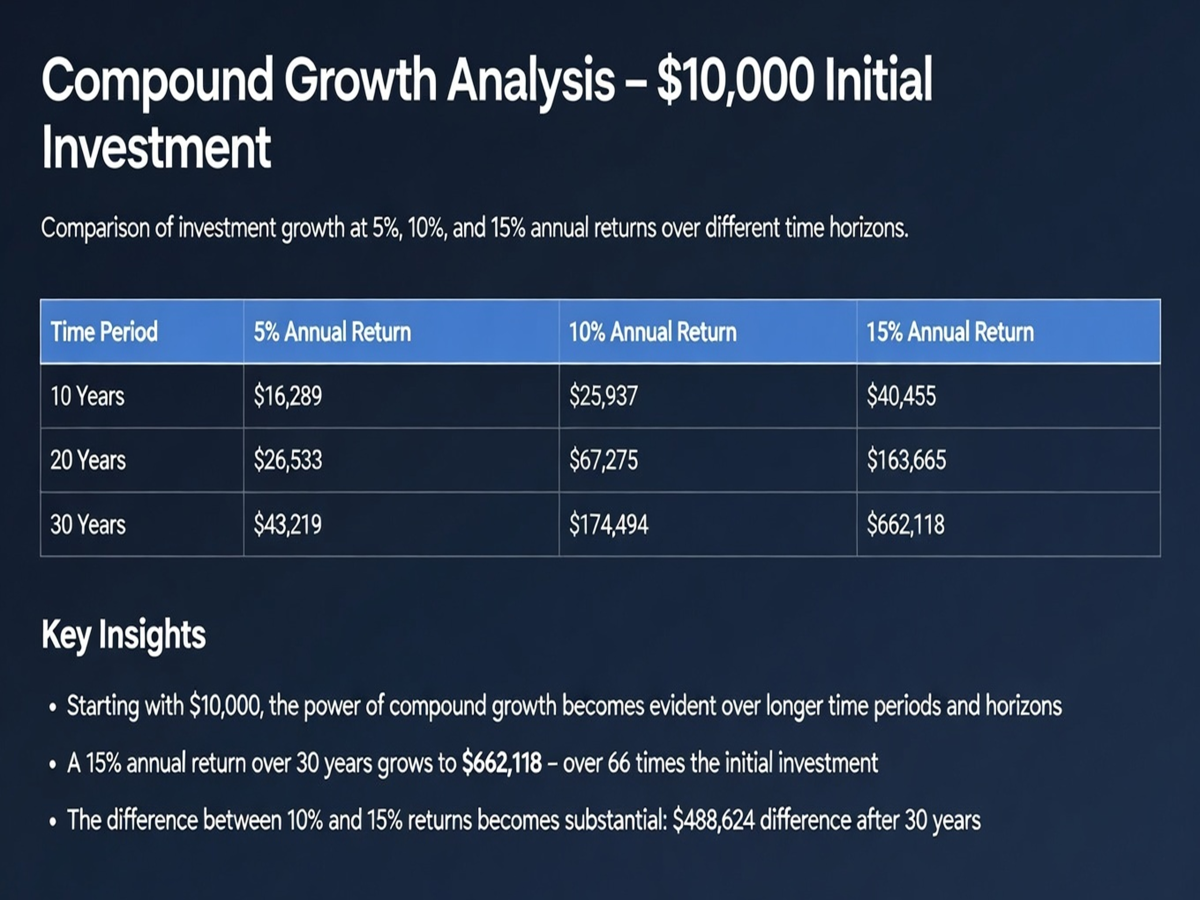

The table below shows the power of compounding at various performance levels for various durations, which I thought you might find informative.

In summary, Markets have demonstrated remarkable adaptability this week. As always, focus on fundamentals over noise.